.jpeg)

WHAT IS A SIF?

A Specialised Investment Fund (SIF) is a type of mutual fund in India that allows more advanced strategies than regular mutual funds.

It sits between:

• Regular Mutual Funds (simple & retail-friendly)

• Portfolio Management Services (PMS) (more aggressive & customised)

Even though it can use strategies like short-selling, derivatives, and higher leverage, it is still officially regulated by the Securities and Exchange Board of India (SEBI) under the SEBI (Mutual Funds) Regulations, 1996 (with 2025 amendments creating this new category).

WHY THIS MATTERS

Because it’s structured as a mutual fund, you still get:

• Transparency – Regular NAV updates

• Regulation – Oversight by Trustees and SEBI

• Tax treatment – Usually taxed as capital gains (like equity/debt funds)

In one line:

A SIF is a regulated mutual fund with more flexibility — meant for comfortable investors taking a little more risk.

WHY DO SIFS EXIST? (THE INVESTMENT GAP)

Before the introduction of SIFs, Indian investors faced a binary choice:

1. Standard Mutual Funds:

• Entry: Low barrier (SIPs from ₹500).

• Limitation: Managers are mostly "long-only" (can only buy stocks) and cannot easily protect capital when markets crash.

2. PMS (Portfolio Management Services) & AIFs (Alternative Investment Funds):

• Entry: High barrier (₹50 Lakh for PMS, ₹1 Crore for AIF).

• Advantage: Flexible strategies (long-short, leverage).

The SIF Solution:

SIFs fill this gap by offering sophisticated strategies with a ₹10 Lakh minimum ticket size. This democratizes access to hedge-fund-like strategies for the "mass affluent" investor who finds PMS too expensive but wants more than a plain vanilla mutual fund.

HOW SEBI CLASSIFIES SPECIALISED INVESTMENT FUNDS (SIFS)

The Securities and Exchange Board of India (SEBI) categorises Specialised Investment Funds (SIFs) into three main types based on their investment focus: Equity, Debt, and Hybrid. Within these categories, SEBI permits seven specific investment strategies designed to offer investors diversified exposure with controlled risk.

EQUITY-ORIENTED SIFS

These funds invest at least 80% of their portfolio in equity instruments. They are allowed to take short positions (selling securities they do not own, aiming to buy them back later at a lower price) up to 25% of their portfolio using derivatives, helping to hedge risks or capitalise on market declines.

Permitted Strategies:

- Equity Long-Short Fund: Combines buying (long) and selling (short) of large, mid, and small-cap stocks to generate returns regardless of whether markets rise or fall.

- Equity Ex-Top 100 Long-Short Fund: Invests at least 65% in companies outside the top 100 by market capitalisation, focusing primarily on mid and small-cap stocks.

- Sector Rotation Long-Short Fund: Concentrates investments in up to four sectors at a time, adjusting sector exposure based on market cycles to optimise returns.

DEBT-ORIENTED SIFS

These funds primarily invest in fixed-income securities such as bonds. They may use derivatives to manage interest rate fluctuations and credit risk effectively.

Permitted Strategies:

- Debt Long-Short Fund: Holds long-term bond positions while taking short positions up to 25% to navigate changing interest rate environments.

- Sectoral Debt Long-Short Fund: Invests across at least two debt sectors but limits exposure to any single sector to a maximum of 75%.

HYBRID SIFS

Hybrid funds invest across multiple asset classes, including equity, debt, Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), and occasionally commodities. These funds adopt flexible investment approaches to balance risk and return.

Permitted Strategies:

- Active Asset Allocator Long-Short Fund: Dynamically shifts allocations among asset classes based on market outlook and opportunities.

- Hybrid Long-Short Fund: Maintains at least 25% allocation each in equity and debt, employing hedging techniques to limit downside risk.

KEY FEATURES (EFFECTIVE 2026)

- Minimum Investment: ₹10 lakh

- Short Exposure Limit: Up to 25% unhedged

Redemption Frequency:

- Equity SIFs: Daily

- Debt SIFs: Weekly

- Hybrid SIFs: Twice a week

Taxation:

- Equity SIFs: Taxed like equity capital gains (with applicable long-term and short-term capital gains rates)

- Debt SIFs: Taxed according to individual income tax slabs

- Hybrid SIFs: Tax treatment depends on the asset allocation structure

BENEFITS OF SIFS

• Smarter investing tricks — Fund managers can use advanced moves like betting on stocks going up and down (long-short), plus tools to protect your money — regular mutual funds mostly just buy and hold.

• Make money even when markets drop — Short positions let the fund possibly earn when prices fall, not just when they rise.

• More ways to spread your money — Invest across stocks, bonds, mixes, and some special areas for better balance.

• Extra protection in bad times — Hedging and smart tools help reduce big losses when things get rough.

• Safe and tax-friendly — Fully watched by SEBI (India's market regulator), with the same easy tax rules as regular mutual funds.

• Not too expensive to join — Starts at ₹10 lakh — a step up from normal funds, but much lower than fancy private options (PMS needs way more).

RISKS OF SIFS

Bigger ups and downs — Prices can swing more wildly than in simple mutual funds.

• Needs ₹10 lakh to start — Not small money; you have to be ready to put in a good amount.

• Depends a lot on the manager — If the fund manager makes wrong calls, it can hurt your returns badly.

• Tools can make losses bigger — Those fancy derivatives boost gains... but also make losses worse if wrong.

• Harder to take money out — Some let you withdraw only weekly or twice a week, not every day.

• Not for everyone — Too complicated and risky if you're new to investing or like super-safe options.

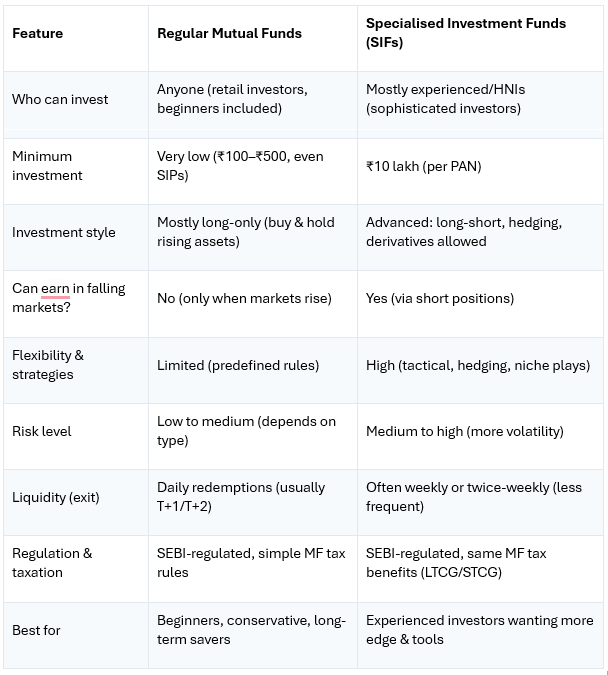

SIFS VS MUTUAL FUNDS: KEY DIFFERENCES EXPLAINED

HOW TO INVEST IN SIFS (STEP-BY-STEP)

1. KYC Compliance: Ensure your Central KYC (CKYC) is updated with your current PAN and Aadhaar.

2. Verify Eligibility: Confirm you meet the ₹10 Lakh minimum ticket size per AMC.

3. Read the SID: Download the Scheme Information Document. Read the "Investment Strategy" and "Risk Factors" sections carefully.

4. Check Costs: Compare the Total Expense Ratio (TER). Lower is better.

5. Understand Liquidity: Check if it is an Interval Fund or has a Lock-in period.

6. Start Small: Allocate only 5–10% of your portfolio initially.

FREQUENTLY ASKED QUESTIONS (FAQS)

Q: Is a SIF a mutual fund?

A: Yes. In India, SIFs are a specific category under SEBI Mutual Fund Regulations, but they have distinct rules for minimum investment (₹10 Lakh) and strategy.

Q: Is a SIF "safe"?

A: Regulated does not mean risk-free. SIFs are regulated by SEBI (so they aren't scams), but they carry high strategy risk and market risk. You can lose capital.

Q: What is the minimum investment for a SIF?

A: The typical regulatory minimum is ₹10 Lakh per investor per AMC.

Q: Can beginners invest in SIFs?

A: While legally allowed, it is not recommended. Beginners should master standard mutual funds first.

Q: How do I track returns?

A: Returns are reported as NAV (Net Asset Value). Use XIRR for SIPs and CAGR for lump sums. Always compare performance against the fund's specific Benchmark (e.g., Nifty 50 Hybrid Composite), not just the Sensex.

FINAL THOUGHTS

Specialised Investment Funds (SIFs) add advanced strategies to India’s investment landscape, but they aren’t for everyone. Build a strong core portfolio first, and consider SIFs only if you understand the risks and have sufficient capital.

DISCLAIMER:

This content is for educational purposes only and is not investment, tax, or legal advice. Mutual fund investments are subject to market risks. Read all scheme documents carefully and consult a SEBI-registered investment adviser before investing.

Disclaimer

What's Trending

Futures & Options: The Market’s Best-Kept Open Secret for Smart Traders

September 12, 2025

How the Rich Use Loans Against Mutual Funds for Lifestyle

January 27, 2026

Union Budget 2026–27 Decoded: Key Takeaways for Smart Investors

February 20, 2026

Top 5 Stocks in the Spotlight This Quarter: A Beginner's Guide

September 25, 2025

Recent Blog

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.