WHAT IS AN AIF? A SMART WAY TO DIVERSIFY WEALTH

If you’ve mastered stocks and mutual funds, you might be looking for the next step in growing your wealth. Enter Alternative Investment Funds (AIFs).

AIFs have emerged as a powerful tool for sophisticated investors aiming for higher long-term growth. But what exactly are they?

In simple terms, think of an AIF as a private investment pool. Unlike mutual funds that are open to everyone and mostly buy public stocks, AIFs are exclusive vehicles where select investors pool money to access opportunities that regular funds usually can't touch.

WHERE DOES THE MONEY GO?

Instead of just buying shares of companies listed on the stock exchange, AIFs invest in "alternative" assets. This includes:

• Startups & Private Companies: Investing in the next big unicorn before it goes public.

• Real Estate Projects: Funding large-scale commercial or residential developments.

• Private Debt: Lending flexible capital to growing businesses.

• Advanced Strategies: Using complex trading methods similar to hedge funds.

WHO IS IT FOR?

AIFs are designed for a specific type of investor. They are best suited for those who:

• Want to diversify their portfolio beyond the volatility of the stock market.

• Are comfortable locking in their money for the long term (often 3 to 7 years).

• Understand that higher potential returns always come with higher risks.

Is It Regulated?

Yes.

Even though they invest in private assets, all AIFs in India operate under the strict supervision of the Securities and Exchange Board of India (SEBI). This ensures a structured, compliant, and transparent environment for investors.

WHO CAN INVEST IN AIFS?

You might be wondering, "Can anyone just sign up for an AIF?" The short answer is no. It is an exclusive club.

Because AIFs take higher risks and lock your money away for longer periods, SEBI mandates a minimum investment of ₹1 Crore per investor. Due to this high entry threshold, AIFs are specifically designed for:

• High-Net-Worth Individuals

• Ultra-HNIs

• Institutional Investors

• NRIs and Foreign Investors

Important Note: Retail investors are not permitted to invest in AIFs. This asset class is strictly for those with a larger portfolio and a higher risk appetite.

TYPES OF AIFS: CHOOSE YOUR FLAVOUR

Not all AIFs are the same. In India, SEBI groups them into three categories based on where they invest and the risk they take.

1. Category I: The "Growth" Funds

• What they do: Invest in startups, small businesses, and infrastructure. Think of this as planting seeds for the future.

• Best for: Investors who want to support innovation and aim for long-term growth.

2. Category II: The "Private" Funds

• What they do: The most common type. They invest in established private companies (Private Equity) or lend money (Private Debt) without borrowing to trade.

• Best for: Investors looking for steady growth from the private market.

3. Category III: The "Complex" Funds

• What they do: Use advanced strategies like hedge funds. They trade rapidly and can borrow money (leverage) to boost returns.

• Best for: Sophisticated investors who want aggressive returns and can handle high risk.

PROS AND CONS OF AIFS

Like any financial product, AIFs have their strengths and weaknesses.

The Benefits

• Higher Return Potential: You get access to private deals and alternative investments that are simply unavailable to retail investors.

• Portfolio Diversification: Private assets often don't move in sync with the stock market, reducing your dependence on traditional equity and debt.

• Professional Management: Your capital is actively managed by experienced fund managers who specialise in these niche areas.

• Market-Independent Strategies: Some AIFs (especially Category III) can generate returns even when the market is falling.

The Drawbacks

• High Entry Barrier: The ₹1 Crore minimum investment keeps most investors out.

• Low Liquidity: This is the "Hotel California" rule, you can check in, but you can't leave easily. Long lock-in periods restrict early exits.

• Higher Risk: Especially in Category I (startups) and Category III (leverage), the risk of capital loss is real.

• High Fees: Management and performance fees can significantly reduce your net returns.

• Limited Transparency: Unlike mutual funds that declare a daily NAV, private assets are harder to value, so disclosures are less frequent.

WHAT’S THE BILL? UNDERSTANDING AIF CHARGES

Before investing, it is critical to understand the costs involved. AIFs typically have a higher fee structure than mutual funds.

1. Management Fee (The Annual Cost): A fixed fee paid to the fund manager every year for managing your money.

Typical Cost: 1% – 2% of your investment.

2. Performance Fee (The Profit Share): A bonus paid to the manager only if they deliver high returns above a set target (called the Hurdle Rate).

Typical Cost: 10% – 20% of the excess profits.

3. Exit Load (The Penalty): A fee charged if you manage to withdraw your money before the agreed lock-in period ends.

4. Operational Charges: Additional costs for legal, audit, and custodian services, which are deducted directly from the fund’s assets.

The Bottom Line: AIFs offer higher return potential, but they come with higher costs. Ensure the potential rewards justify the fees!

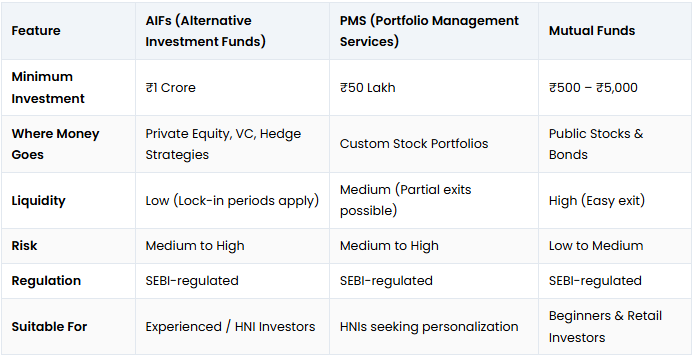

AIFS VS. PMS VS. MUTUAL FUNDS: KEY DIFFERENCES

Here’s how AIFs compare at a glance.

FINAL TAKEAWAY:

Consider AIFs if you have ₹1 Crore+, patience for long lock-ins, and high risk tolerance. They are powerful tools for diversifying beyond traditional markets.

DISCLAIMER:

This content is for educational purposes only and does not constitute investment advice. AIFs involve market and liquidity risks. Please consult a qualified financial advisor before investing.

Disclaimer

What's Trending

FIFA World Cup 2026: 3 Investment Angles for India

June 10, 2026

Recent Blog

.jpeg)

.jpeg)

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.