WHAT IS PMS?

A WAY TO MANAGE WEALTH

Portfolio Management Services (PMS) is a professional investment service where qualified portfolio managers handle your money based on your financial goals and risk tolerance.

Unlike Mutual Funds, where you buy units of a pooled fund, PMS investment offers direct ownership of stocks and securities in your own Demat account. This makes it a more personalised and transparent approach for investors who want focused wealth creation.

WHO CAN INVEST IN PMS?

MINIMUM INVESTMENT REQUIRED

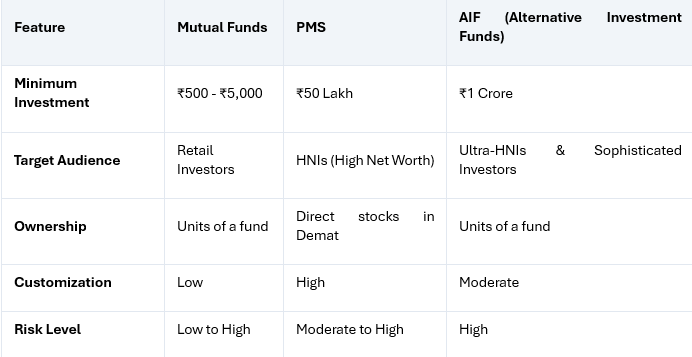

In India, the Securities and Exchange Board of India (SEBI) mandates a minimum investment of ₹50 Lakh.

Because of this high entry requirement, PMS is specifically designed for High-Net-Worth Individuals (HNIs) who have significant capital to invest and are looking for professional management.

TYPES OF PMS

CHOOSE YOUR LEVEL OF INVOLVEMENT

There are three main types of PMS, depending on how much control you want:

1. DISCRETIONARY PMS

• How it works: The portfolio manager makes all the investment decisions (buying and selling) on your behalf.

• Your role: You do not need to approve every trade. You simply track the performance.

• Best for: Investors who want a completely hands-off experience.

2. NON-DISCRETIONARY PMS

• How it works: The manager suggests investment ideas, but they cannot execute the trade without your permission.

• Your role: You have the final say on every buy or sell decision.

• Best for: Investors who want expert advice but prefer to keep control.

3. ADVISORY PMS

• How it works: The manager only provides investment advice and recommendations.

• Your role: You execute the trades yourself based on their advice.

• Best for: Active investors who want professional guidance but handle their own execution.

PROS AND CONS OF PMS

THE BENEFITS

• Professional Management: Your money is managed by experienced professionals who actively track the market.

• Customisation: Portfolios can be tailored to your specific financial goals (e.g., high growth vs. stability).

• Direct Ownership: You hold the stocks in your own Demat account, offering better transparency than mutual funds.

• Transparency: You get detailed reporting on every transaction, fee, and holding.

THE DRAWBACKS

• High Entry Barrier: The ₹50 Lakh minimum investment makes it inaccessible for small investors.

• Higher Fees: Management and performance fees can be higher than standard mutual funds.

• Tax Implications: Since you own the stocks directly, you are responsible for paying capital gains tax on every profitable trade the manager makes.

• Concentration Risk: PMS portfolios often hold fewer stocks than mutual funds, which can lead to higher volatility (sharper ups and downs).

PMS CHARGES EXPLAINED

UNDERSTANDING THE COSTS

Before investing, it is critical to understand the fee structure:

1. Management Fee: A fixed annual fee (typically 1% to 2.5%) charged on the total value of your portfolio for the service.

2. Performance Fee: A "profit-sharing" fee. If the manager beats a certain benchmark (e.g., 10% return), they charge a percentage (typically 15% to 25%) of the excess profit.

3. Exit Load: A penalty charged if you withdraw your money early (usually within the first 1-3 years).

4. Operational Charges: Standard costs like brokerage, custodian fees, and taxes (GST, STT) are deducted from your portfolio.

COMPARISON: PMS VS. MUTUAL FUNDS VS. AIF

COMMON INVESTMENT STRATEGIES

HOW MANAGERS GROW YOUR MONEY

• Growth Strategy: Investing in companies expected to grow faster than the average market.

• Value Strategy: Buying quality stocks that are currently undervalued or "cheap."

• Multicap Strategy: A mix of large, mid, and small-sized companies.

• Small-Cap Strategy: Focusing on smaller companies with high growth potential (higher risk).

• Multi-Asset Strategy: Investing in a mix of stocks, debt, and gold to balance risk.

WHO SHOULD CHOOSE PMS?

PMS is suitable if you:

• Have a surplus of ₹50 Lakh or more to invest.

• Lack the time or expertise to track the stock market daily.

• Want a personalised portfolio rather than a generic mutual fund.

• Understand that higher returns often come with higher risks and volatility.

RISKS YOU SHOULD UNDERSTAND BEFORE CHOOSING PMS

While PMS offers personalised management, it is important to understand the risks involved before investing.

• Market Risk: PMS investments are subject to market fluctuations. Portfolio values can fall during market downturns.

• Concentration Risk: PMS portfolios often hold fewer stocks than mutual funds. If a few investments perform poorly, the impact can be significant.

• Manager Risk: The performance of your portfolio depends heavily on the portfolio manager’s decisions and strategy.

• Liquidity Risk: Some stocks may not be easy to sell quickly during volatile markets.

• Tax Timing Risk: Frequent buying and selling can trigger short-term capital gains tax.

Understanding these risks helps set realistic expectations.

FINAL TAKE

Choosing a PMS isn’t about flashy returns. It’s about trust and fit.

Pick a provider who protects your money during market falls, grows it steadily, explains things clearly, and is registered with the

Securities and Exchange Board of India.

Most importantly, make sure the PMS matches your goals, your risk comfort, and your timeline. When it fits you, investing feels simple and stress-free.

DISCLAIMER

For educational purposes only. PMS investments carry market risks. Please consult a financial advisor and ensure the provider is registered with the Securities and Exchange Board of India before investing.

Disclaimer

What's Trending

Your Wallet Has Four Gears — Learn When to Shift

November 11, 2025

Comprehensive Guide to Understand Face Value Split

July 30, 2024

Recent Blog

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.