.jpeg)

How to Pick a Mutual Fund Without Losing Your Mind

The Problem: Too Many Choices, Too Little Clarity

Walk into an ice cream shop with three flavours. Easy choice.

Open a mutual fund app. 2,000+ options. Large-cap, mid-cap, small-cap, ELSS, gilt, dynamic bond, balanced advantage, flexi-cap, multi-asset, index, sectoral, thematic, liquid, ultra-short, credit risk, corporate bond, floater, banking & PSU... and 15 more categories you've never heard of.

Most people do one of three things:

• Copy a friend's choice

• Pick last year's top performer

• Close the app and postpone the decision

There's a simpler way. Two questions cut through everything.

Question 1: Where Does My Money Go?

Every mutual fund puts your money in one of three places. Everything else is just packaging.

Place A: Stocks (Equity Funds)

Your money buys small pieces of companies — the same ones whose products you use daily.

What happens: When companies do well, your money grows. When they struggle, your money shrinks. Over 7-10 years, this has been India's best wealth builder. But some years, you might see your investment drop 20%. That's normal, not broken.

Real example: ₹3,000 invested monthly for 10 years = ₹3.6 lakh put in. At an average growth of 12%, roughly ₹6.9 lakh comes out. But in year one, you might see ₹36,000 become ₹30,000. The growth isn't linear. It's lumpy.

Good for: Goals 7+ years away. Retirement. Child's college. Buying a home.

Place B: Loans (Debt Funds)

Your money is lent to the government or companies. They pay interest. You earn that interest.

What happens: More flexible than bank FDs. Usually better than savings accounts. But unlike FDs, these can lose money. In 2019, one company's default hurt several debt funds. In 2020, some funds froze investor money for months.

Two simple risks:

• Interest rates go up → old bonds become less valuable temporarily

• Company can't repay → you lose money permanently

Good for: 1-3 year goals. Emergency funds-money you cannot afford to lose.

Place C: Mixed Bag (Hybrid Funds)

Part stocks, part loans. Some keep fixed ratios. Others automatically adjust based on market conditions.

What happens: When stocks drop 15%, these might drop 8%. Less scary. Less growth potential, too.

Good for: 3-5 year goals. First-time investors who want growth without full stock market stress.

Quick Comparison Table

Table

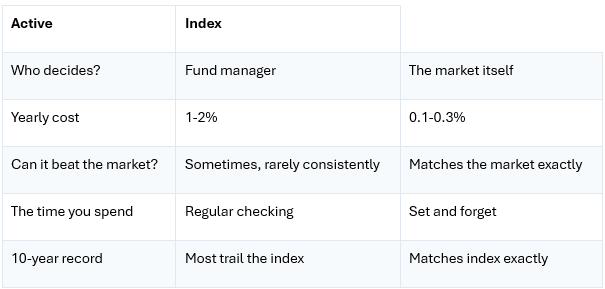

Question 2: What Am I Paying?

Now you know where your money goes. The second question is who gets paid to manage it — and how much.

Option 1: Active Management

A professional picks stocks for you. Tries to beat the market.

Cost: 1-2% per year, quietly removed from your returns.

Reality check: Over 10 years, most active large-cap funds in India failed to beat a simple Nifty 50 index. You paid for expertise. You got average results.

Where it works better: Mid-cap and small-cap stocks. Less crowded. More room for genuine skill to matter.

Option 2: Passive Management (Index Funds)

Your money is split across all 50 companies in the Nifty 50. No expert picking favourites. No "strategy." When the market rises, you rise. When it falls, you fall.

Cost: 0.1-0.3% per year.

Why banks rarely suggest this: No "our expert found this gem" story. Lower commissions.

The Cost Difference: Real Numbers

₹5,000 monthly for 20 years (assuming 12% market growth before fees):

Table

That gap equals a year's salary for many Indians. Or a car. Or three years of school fees.

The "small" fee wasn't small. It was just hidden.

Simple Comparison

Table

Five years ago, hardly anyone talked about them. Today, over ₹10 lakh crore sits in passive funds (as of early 2025).

What changed? Regulators forced funds to show benchmark comparisons. Investors saw that expensive active funds often underperformed cheap index funds. The math became impossible to ignore.

This doesn't mean active funds are useless. It means you pay for skill only where skill has proven itself — mainly in mid-cap and small-cap categories.

Your Decision: A Simple Map

When do you need the money?

• Under 2 years → Loan-based (debt) fund. Safety first.

• 2-5 years → Mixed (hybrid) fund. Automatic balance is worth a slight extra cost.

• 5+ years → Ask yourself: Will I actually review this regularly?

o No → Nifty 50 or Sensex index fund. The right choice for 9 out of 10 people.

o Some → Mostly index, small active mid/small-cap portion.

o A lot → Custom mix. But "a lot" means quarterly reviews, not one Sunday of research.

Most people who think they'll review "a lot" actually won't. That's an expensive mistake.

Do This Now (2 Minutes)

1. Open any fund you own or consider

2. Find "Scheme Information Document" or factsheet

3. Check two things:

• Where does it invest? (Stocks / Loans / Both)

• What's the expense ratio? (Yearly fee percentage)

4. Ask: Does this match my timeline? Is the fee justified?

If these numbers are hard to find, that's intentional. Good products show them clearly.

Remember

• Past returns don't predict future results

• Star ratings change every quarter

• "Exclusive" schemes are rarely exclusive

• Simple usually beats complicated

Two questions. Three places your money can go. Two ways it can be managed. That's the entire map. Everything else is decoration.

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully. Past performance does not guarantee future returns. This is educational content, not investment advice. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

Predict Nothing, Prepare For Everything: The Straddle Way

December 4, 2025

Oil Crisis 2026: Why Your LPG Bill Just Went Up ₹60

March 27, 2026

How to Start SIP Investment Online in 5 Simple Steps

October 28, 2025

Recent Blog

.jpeg)

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.