The Story: When the Bank Sent the Bad News

Meera had locked ₹1,00,000 into her bank FD at 7.5% just a year ago. It felt safe. Predictable. Perfect.

Last month, her bank pinged her with a renewal alert. New FD rates had slipped to 6%. Her old deposit was still earning 7.5% — but only until it matured. When she asked the branch manager what to do next, he shrugged. "That's how FDs work. Rates go down, you earn less."

But Meera wasn't ready to accept less.

A few hours of reading later, she had landed on something her cousins, her colleagues, and even her bank manager rarely brought up — floating rate bonds. The more she read, the clearer it became. This wasn't a gamble. It was simply the smarter shelf to stand on when interest rates were sliding.

What Is a Floating Rate Bond, Really?

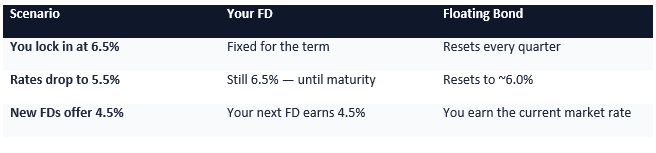

You already know the FD story. You deposit ₹1 lakh with your bank at 6.5%. They promise ₹6,500 in interest. Locked. Safe. Stuck.

A floating rate bond is a loan you give to the government or a company, but the interest rate doesn't stay still. Every three to six months, it resets, based on a market benchmark. Think of the benchmark as the pulse of the economy. When the pulse moves, your interest moves with it.

The structure is simple. Your bond might pay something like a 3-month T-bill rate + 0.5%. The T-bill rate is just the interest the government pays on its short-term borrowing. The "+0.5%" is your spread — your kicker on top of the benchmark.

When the T-bill is at 7.0%, you earn 7.5%. If it drops to 6.0% next quarter, you earn 6.5%. If it rises to 7.5%, you earn 8.0%.

Your FD is frozen in time. Your floating bond moves with the market.

Why 2026 Is the Year This Matters

The Reserve Bank of India has been cutting interest rates to support economic growth. Bank FD rates have been quietly trending lower for months. Most economists expect this rate-cutting cycle to continue through 2026.

The question for any saver isn't "Will FD rates fall?" It's "How do I protect myself when they do?"

A floating bond doesn't stop rates from falling — nothing does. What it stops is the slow bleed of renewing into a worse deal. There's also a quiet bonus: when overall rates fall, the bond's resale price usually rises in the secondary market. An FD's value never moves — it's worth what you put in.

The Real-Money Math, in One Clean Example

Theory is fine. Numbers are clearer.

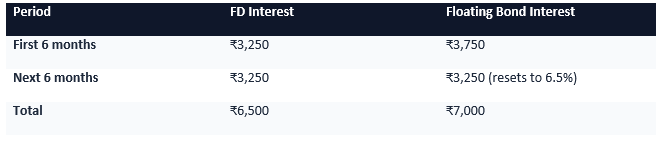

Imagine you put ₹1,00,000 into either option in early 2026:

Option A — Bank FD at 6.5%, fixed for one year.

Option B — Floating bond paying 3-month T-bill + 0.5% (so 7.5% to start, with the T-bill at 7.0%).

Now suppose rates fall by 1% halfway through the year — the most likely 2026 scenario.

Your floating bond earned ₹500 more on the same ₹1 lakh — about 7.7% better in actual rupees. And if rates were to rise instead of fall, the floating bond would have pulled even further ahead.

These figures are illustrative. Real returns depend on the issuer, the actual benchmark movement, and what the bond is trading at when you exit. The principle, though, is real.

The Honest Pros and Cons

The good:

Rate protection. When rates fall, your coupon adjusts gracefully. You're not stuck on yesterday's number.

You also win in rising rates. If the cycle reverses, your coupon climbs. FDs can't do that.

A formula you can read. "T-bill + 0.5%" is transparent — no surprises buried in fine print.

Multiple shelves. Government, bank, and corporate issuers — pick by your risk appetite.

Possible price gain on exit. When rates fall, the bond's market price often rises. A small bonus on top of the interest, if you sell.

The honest other side:

Falling coupons hurt too. Your payout drops when rates drop. The bond protects you from being frozen at a bad rate, not from rates falling at all.

Price swings on early exit. Sell before maturity, and the price could be lower than you paid. Hold to maturity, and your principal is intact (assuming no default).

Liquidity isn't promised. Government and large bank bonds usually trade actively. Smaller corporate bonds can be hard to sell quickly.

Credit risk on corporates. Unlike a bank FD (covered up to ₹5 lakh under DICGC deposit insurance), bonds carry the full risk of the issuer. A weak company can default.

Higher entry tickets. Some bonds start at ₹10,000; others want ₹1,00,000 or more. Check before buying.

Who Issues Them, and How They're Taxed

Three rough buckets:

Government bonds — issued by the RBI / Government of India. Lowest risk, lowest return. The cleanest starting point for a first-time bond buyer.

Bank bonds — safer than corporate, riskier than government. Important caveat: bank FDs are insured up to ₹5 lakh; bank bonds are not.

Corporate bonds — higher returns, higher risk. Always check the credit rating (AAA is safest) before buying.

On tax, the rule is simple. Floating bond interest is added to your total income and taxed at your slab — 5%, 20%, or 30%, depending on your bracket. There's no special bond-only tax break. If your annual interest crosses ₹40,000, TDS at 10% kicks in automatically. The issuer handles it; you don't have to do anything extra.

How to Buy: A Five-Step Walkthrough

First — pick your type. Government for safety, bank for balance, corporate for yield.

Second — get KYC done. PAN, Aadhaar, address proof, and bank details. Most brokers do this online in five minutes.

Third — open a demat account. Floating bonds sit in a demat account the same way stocks do.

Fourth — read the bond's details. Note the benchmark (3M T-bill, repo, MIBOR), the spread, the maturity date, and the reset frequency.

Fifth — check liquidity and place the order. Ask your broker if there's an active secondary market for that bond. Then buy through the app, just like a stock.

Who This Is For — and Who Should Wait

This product fits well if you're a working saver who can park money for one to three years, you expect rates to keep softening through 2026, and you can stay calm if the bond's price wobbles between resets. It's a useful diversifier on top of an existing FD pile.

It's the wrong tool if you might need that money back in six months, you're a panic-seller when prices dip, you're considering a small corporate bond from a company you don't really know, or you've never invested before and want zero moving parts.

The Bottom Line

Floating-rate bonds aren't a magic upgrade to your FD. They won't guarantee higher returns. They won't protect you from every kind of risk.

But they do one thing FDs structurally can't — they move with the market. In a year when rates are widely expected to slide, that single feature can quietly add up.

A balanced way to think about it: don't replace your FDs. Sit floating bonds next to them. A common framework is FDs for safety and predictability, floating bonds for rate flexibility, and a small slice of cash for emergencies. The exact split depends on your goals, your age, and your comfort with movement.

Start small. Read the offer document. Ask the questions your bank manager won't volunteer. Then decide.

FAQs

How is a floating rate bond different from an FD?

A floating bond's interest resets every three to six months based on a market benchmark. An FD's rate is fixed for the full term. In a falling-rate environment, the floating bond's coupon also drops, but the FD silently leaves you stuck at today's lower rate when you renew.

Can I lose money in a floating rate bond?

If you hold to maturity and the issuer doesn't default, you get your full principal back. If you sell before maturity in the secondary market, the price can be higher or lower than what you paid, so a loss on early exit is possible.

How often do the coupons reset?

Most are reset quarterly or semi-annually. The exact schedule is in the offer document.

What if rates keep falling through 2026?

Your coupon will keep stepping down with each reset. The trade-off is that the bond's secondary market price usually rises in a falling-rate environment, so a planned early exit could earn you a small capital gain on top of the interest.

Are there small-ticket floating bonds?

Yes. Many start at ₹10,000. Government-issued floating bonds typically have lower minimums than corporate ones.

Is now a good time to buy?

With rates expected to keep softening, this isn't a bad window. But these are not products to time perfectly — they're meant to be held. What matters more is whether you understand the bond, the issuer, and your own holding horizon.

Where GoPocket Fits

GoPocket gives you a single demat account that already holds your stocks, mutual funds, ETFs, and IPOs — and floating rate bonds will sit on the same shelf. One login, one paperwork, no running between branches. If you don't have a demat account yet, opening one takes about five minutes and keeps you ready for the moment a good floating bond shows up on your radar.

DISCLAIMER

This blog is for educational purposes only and does not constitute investment, tax, or legal advice. All examples, scenarios, and rate figures are illustrative — actual returns depend on the issuer, the benchmark, the prevailing market rate at each reset, and the price at which you exit. Floating rate bonds carry credit risk (especially corporate bonds), liquidity risk, and interest-rate risk. Unlike bank FDs, they are not covered by deposit insurance. Past performance is not indicative of future results. Tax treatment depends on your individual income slab. Investments in the securities market are subject to market risks; please read all related documents carefully before investing. Readers are strongly encouraged to consult a SEBI-registered investment adviser before making any investment decision. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

Wings Of Growth - Gopocket's Journey

July 8, 2025

Recent Blog

.jpeg)

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

.png)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.