When most people need money for lifestyle expenses – a vacation, new gadgets, education, a wedding, or an emergency – their first thought is to sell their mutual fund investments or stop their SIPs.

But wealthy investors don’t do that.

Instead of breaking their investments and losing future wealth, the rich borrow against mutual funds.

This strategy is known as a Loan Against Mutual Funds (LAMF) – and it explains how financially smart people fund lifestyle needs without sacrificing long-term wealth creation.

WHY SELLING MUTUAL FUNDS CAN BE A COSTLY FINANCIAL MISTAKE

When you redeem mutual fund investments to meet expenses, you create multiple financial losses:

• You stop compounding, which reduces long-term growth

• You may have to pay capital gains tax

• You permanently lose the future earning potential of that invested money

• You shrink your long-term wealth corpus

The biggest loss is often invisible – the wealth that money could have created if left invested.

Wealthy investors avoid redeeming mutual funds because they treat them as long-term wealth engines rather than short-term cash reserves,choosing avoid selling mutual funds as a core principle.

WHAT IS A LOAN AGAINST MUTUAL FUNDS (LAMF)?

A Loan Against Mutual Funds allows you to borrow money by pledging your mutual fund units as collateral, without selling them.

Here’s how it works:

• Your mutual fund investments remain fully invested

• You receive a loan based on a percentage of your portfolio value

• Your money continues to earn market-linked returns

• You pay only interest every month

• You can repay the principal anytime, without strict EMI pressure

In simple terms:

You get cash for your needs, but your investments keep growing.

This is why LAMF is seen as a smarter alternative to selling investments.

Why the Rich Prefer Borrowing Instead of Selling Investments

Wealthy investors follow a practical financial rule:If your investment returns are higher than your loan interest rate, selling investments makes no sense.

Typically:

• Mutual funds may generate 10–12% or higher long-term returns

• Loans against mutual funds usually carry around 9–11% interest

If investments grow faster than the loan cost, then borrowing preserves wealth while selling destroys future potential.

So instead of interrupting compounding, smart investors use leverage responsibly and allow their money to keep growing.

REAL-LIFE LIFESTYLE FUNDING SCENARIO EXPLAINED IN THE ARTICLE

The reference article describes a real-world scenario where a person needs money for a lifestyle expense.

The person evaluates multiple options:

• Option 1: Using a Credit Card

Credit cards often charge extremely high interest (up to 36–48%)

This can easily lead to a debt trap

• Option 2: Taking a Personal Loan

Personal loans have higher interest rates

Fixed EMIs can create monthly financial pressure

• Option 3: Selling Mutual Funds

Stops compounding

Triggers capital gains tax

Reduces long-term wealth

• Option 4: Loan Against Mutual Funds (Smart Choice)

Lower interest compared to unsecured loans

No need to sell investments

Investments continue to grow

Flexible repayment

The article shows that borrowing against mutual funds is often the most financially efficient option.

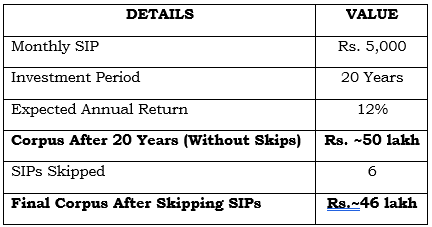

WHY SKIPPING SIPS CAN QUIETLY DESTROY LONG-TERM WEALTH

Another key insight from the article is the hidden danger of skipping SIPs.

Many investors believe skipping SIPs for a few months is harmless – but the long-term impact can be surprisingly large.

Now recalculated using your requirement: Rs.5,000/month SIP

Impact of Skipping SIPs (Rs.5,000/month Example)

What This Means

Skipping just 6 SIPs results in a loss of Rs.3+ lakh, even though the skipped investment amount is only Rs.30,000.

The real damage is the impact of skipping SIP, where the SIP compounding loss quietly grows over long periods.

This reinforces a core message from the article:

Consistency matters more than the size of your investment.

WHY LOAN AGAINST MUTUAL FUNDS IS BETTER THAN OTHER BORROWING OPTIONS

Compared to Credit Cards

• Credit card interest can go as high as 48% per year

• LAMF offers much lower interest, reducing financial strain

COMPARED TO PERSONAL LOANS

Personal loans require fixed EMIs

LAMF allows flexible repayment

No heavy income documentation required

COMPARED TO A LOAN AGAINST PROPERTY

Property loans require long processing times

More paperwork and collateral

LAMF is faster, simpler, and mostly digital

KEY BENEFITS OF LOAN AGAINST MUTUAL FUNDS

No need to redeem or sell investments, helping investors avoid selling long-term investments

• No need to redeem or sell investments

• Lower interest compared to unsecured loans

• No fixed EMI obligation

• Pay only interest monthly

• Repay principal anytime

• No foreclosure or prepayment charges

• Fully digital and quick approval process

• Works even if your credit score is average

• Investments continue to compound normally

These benefits explain why LAMF is becoming a preferred option among financially savvy investors.

WHEN DOES THIS STRATEGY MAKE FINANCIAL SENSE?

According to the article, this strategy works best when:

• You need short-term liquidity

• You want to avoid selling long-term investments

• Your mutual funds are expected to outperform the loan interest

• You want to avoid tax and compounding loss

However, it also emphasises that this should not be used for reckless or impulsive spending – it works best for planned financial needs.

THE CORE WEALTH LESSON FROM THE RICH

The rich don’t build wealth by:

• Panic-selling investments

• Stopping SIPs frequently

• Breaking compounding cycles

They build wealth by:

• Staying invested

• Borrowing strategically

• Preserving long-term growth, instead of interrupting compounding, smart investors use leverage responsibly and let their money

• Making logical financial decisions instead of emotional ones

Their advantage isn’t just money –

It’s discipline, patience, and smarter financial thinking.

FINAL THOUGHT

If your goal is to enjoy your lifestyle without damaging your future wealth,

The smarter approach is not selling investments – but using them strategically.

Because the true secret of long-term wealth is simple:

Never interrupt money that is already growing.

Disclaimer

What's Trending

Market Outlook: Week Ahead (March 23–27, 2026)

March 23, 2026

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.