As health needs evolve and insurance offerings change, many policyholders consider moving to better plans. But what holds them back is the fear of losing accumulated benefits like waiting periods, bonuses, and claim history. Fortunately, the Insurance Regulatory and Development Authority of India (IRDAI) offers a solution: health insurance porting.

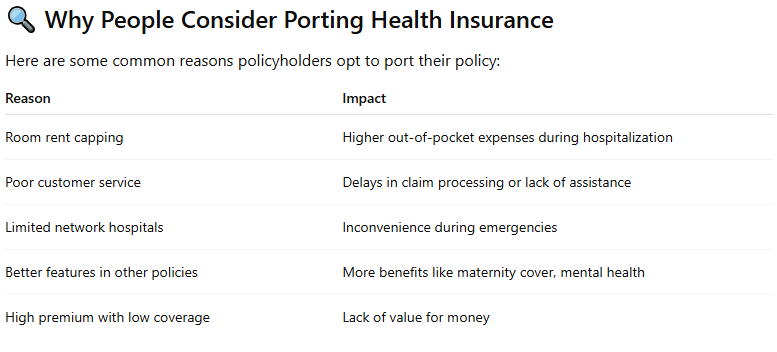

Health insurance porting empowers you to switch to a new insurer without forfeiting benefits you’ve earned. If your current policy has restrictive clauses—like room rent caps, sub-limits on treatments, or exclusions for pre-existing diseases—porting can provide significant relief.

Let’s decode the process, eligibility, benefits, and key mistakes to avoid while switching health insurance in 2025.

What is Health Insurance Porting?

Health insurance porting refers to transferring your existing health insurance policy from one insurance provider to another without losing your policy’s continuity benefits. This includes:

- Waiting periods for pre-existing diseases

- No-claim bonuses (NCBs)

- Time-bound coverages like maternity benefits

This feature ensures that policyholders are not penalized for switching insurers, especially if they’re unhappy with current terms or coverage limitations.

When Can You Port Your Health Insurance?

Porting is not allowed at any random time during the policy year. You must initiate the portability request at least 45 days before the renewal date of your existing policy.

Example:

If your policy expires on July 31st, you should apply for porting by mid-June.

Step-by-Step Guide to Porting Your Health Insurance in 2025

Switching your insurer can be smooth if you follow these steps:

Step 1: Compare Policies Across Insurers

Use IRDAI-approved aggregators or consult advisors to find policies with:

- No room rent limits

- Higher disease-specific sub-limits

- Broader pre-existing disease cover

- Shorter waiting periods

Look for plans that support chronic conditions like diabetes, hypertension, and lifestyle diseases.

Step 2: Notify Your Existing Insurer

Inform your current insurer in writing about your decision to port. Most insurers now offer this via online portals.

Step 3: Apply to the New Insurer

Fill out the portability request form and proposal form of the new insurer. Submit with:

- Existing policy copy

- Claim history

- Medical history

Honesty is crucial—non-disclosure of pre-existing diseases like diabetes can lead to rejection or claim denial later.

Step 4: Underwriting by the New Insurer

The new insurer may:

- Accept the policy as-is

- Request medical tests

- Add loading (extra premium) or exclusions

- Reject the proposal (in rare cases)

Step 5: Complete the Transition

Once approved, pay the premium and the new policy will take effect from the renewal date. All previous continuity benefits carry forward.

Common Mistakes to Avoid While Porting

Waiting until the last minute

Start 45-60 days before renewal. Delays can cause rejection or default auto-renewal.

Hiding health conditions

Always disclose full medical history, even if the new insurer doesn’t ask immediately.

Not reading exclusions

Some policies may offer better surface benefits but hide key exclusions. Read fine print.

Choosing solely on premium

A lower premium isn’t always better. Consider network hospitals, claim ratios, and customer service.

Porting and Pre-existing Diseases: What Stays and What Doesn’t?

Here’s how porting works if you have a pre-existing condition:

- If you've already completed 2 years of a 4-year waiting period, the new insurer counts that and only applies 2 more years.

- But, if the new insurer has a shorter waiting period, you may benefit faster.

This continuity is why porting is better than cancelling and buying a fresh policy—especially for people with diabetes, asthma, or hypertension.

Case Example: Room Rent Capping

If your current plan limits room rent to ₹3000/day, but you choose a hospital charging ₹6000/day, you must pay the difference out of pocket—including proportionate charges for nursing, surgeon, etc.

By porting to a plan without such caps, you get full reimbursement for your preferred hospital room type—no compromise during emergencies.

Financial Tip: Pair Insurance Porting with Smart Investing

While insurance covers unexpected health costs, true financial strength comes from long-term investing.

If you're thinking long-term—porting health insurance and avoiding claim rejections—then consider:

- Starting a Systematic Investment Plan (SIP) for health corpus

- Investing in health-focused mutual funds

- Building an emergency fund alongside your coverage

GoPocket: One App for Financial and Health Planning

Managing both insurance and investments? Look no further than GoPocket.

With GoPocket, you can buy insurance at any time click the link below and start protecting your future

Disclaimer

What's Trending

UPI Is Popular! But Do You Know About ULI?

July 22, 2025

The Habit That’s Secretly Eating Your Wealth

August 7, 2025

THE SMELL OF SWEETS AND A HINT OF HOPE

October 16, 2025

Recent Blog

.jpeg)

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.