.jpeg)

SCSS vs Vaya Vandana

₹50 Lakhs. Two Safe Schemes. One Quietly Pays ₹2.1 Lakhs More.

Rajesh retired on a Tuesday. No dramatic farewell — just one small cake in the pantry and 35 years of working life quietly over.

The next Monday, his bank manager placed two brochures on the table. SCSS. Vaya Vandana Yojana.

Both government-backed. Both promise safe, predictable income. Both are marketed as the perfect retirement choice.

And that's exactly where most retirees get stuck.

When two products sound equally safe, people assume the outcome is the same, too. It isn't. One quiet difference between SCSS and Vaya Vandana can change retirement income by ₹2.1 lakhs over five years — and most people never notice it.

In the next few minutes, you'll know more about these two schemes than most bank managers who sell them.

THE FIRST THING YOU NEED TO KNOW

Vaya Vandana Is Already Closed

Before comparing numbers, here is the one fact that changes everything:

The government permanently closed Vaya Vandana Yojana on March 31, 2023. If you didn't invest before that date, you simply cannot get it today — not through LIC, not at any post office, not anywhere.

⚡ What This Actually Means

New retirees in 2026 have one government-backed income scheme available: SCSS.

If you already hold Vaya Vandana (bought before 2023), you own something nobody can buy anymore.

The real question today isn't 'which should I choose?'

It's: 'Is SCSS now the strongest retirement option still standing?'

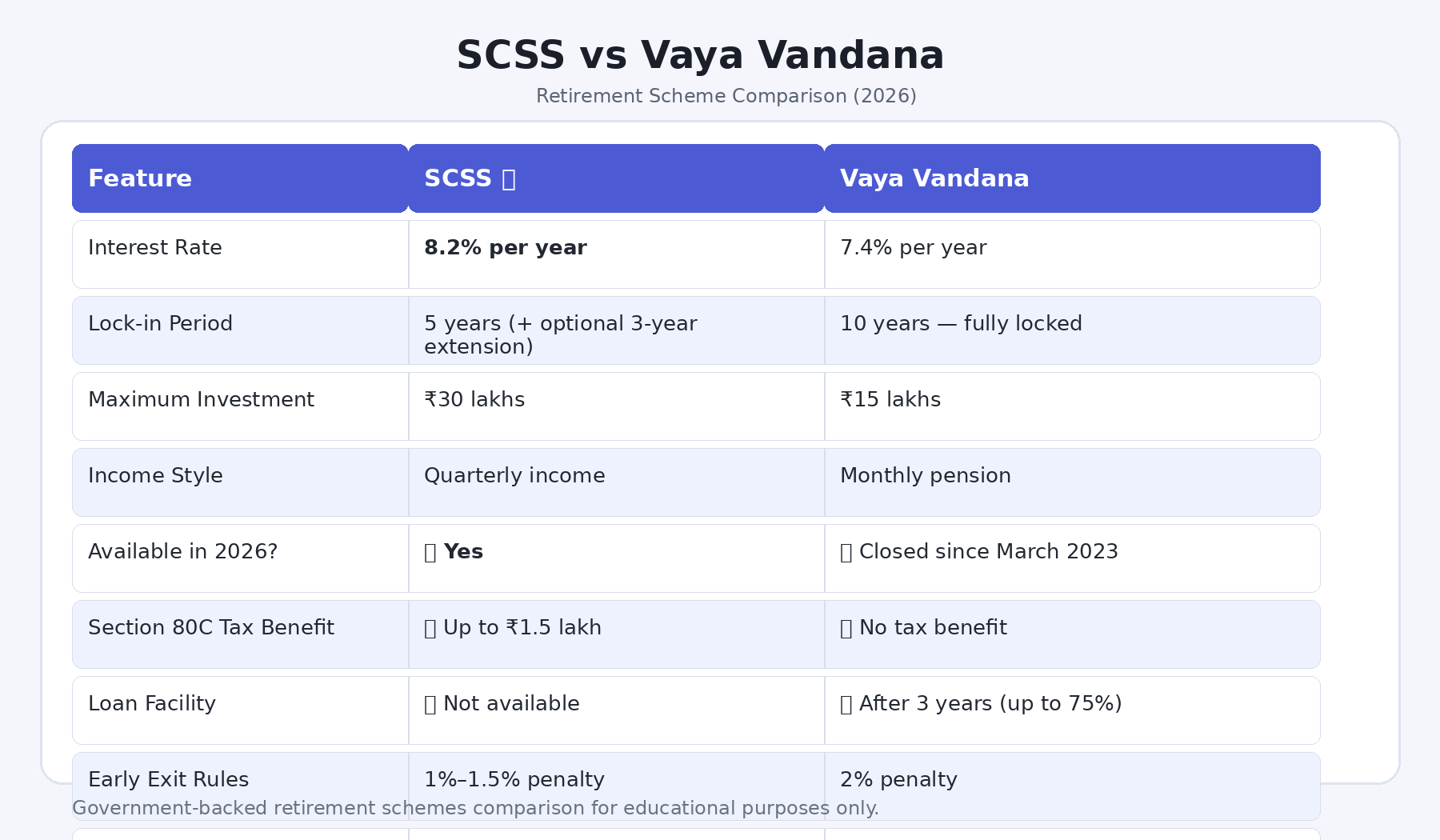

THE NUMBERS THAT ACTUALLY MATTER

What ₹50 Lakhs Earns You

Skip the percentages. Here's what your account actually sees.

SCSS at 8.2%: ₹4,10,000 a year. That's ₹1,02,500 landing in your account every quarter.

Vaya Vandana at 7.4%: ₹3,70,000 a year. Around ₹30,833 every month.

The gap? ₹40,000 a year. Over five years — ₹2 lakhs. Enough for a medical emergency, a family trip, or simply one less financial worry.

Tiny percentages quietly become life-changing numbers in retirement.

And the after-tax picture is even clearer. SCSS gives you a Section 80C deduction of up to ₹1.5 lakhs. Vaya Vandana offers no such benefit. For someone in the 20% tax bracket, that's an extra ₹30,000 saved in year one alone.

The headline difference is 0.8%. The real-money difference is significantly larger.

FULL COMPARISON

Side by Side

THE PART MOST BLOGS MISS

Even 8.2% Has a Silent Enemy

Here's an uncomfortable truth neither scheme mentions upfront.

India's average retail inflation runs at 5–6% a year. Which means:

SCSS real return: 8.2% minus 6% = roughly 2.2%

Vaya Vandana's real return: 7.4% minus 6% = roughly 1.4%

Both schemes protect your principal. Neither one grows your wealth fast enough to beat inflation alone.

That's why smart retirees don't put everything into one basket. A balanced split that actually works:

→ 50–60% in SCSS — your guaranteed, no-stress quarterly income

→ 20–30% in short-duration debt funds — better inflation buffer with low risk

→ 10–20% in diversified equity mutual funds — long-term growth engine

SCSS is your income floor. It isn't the whole house.

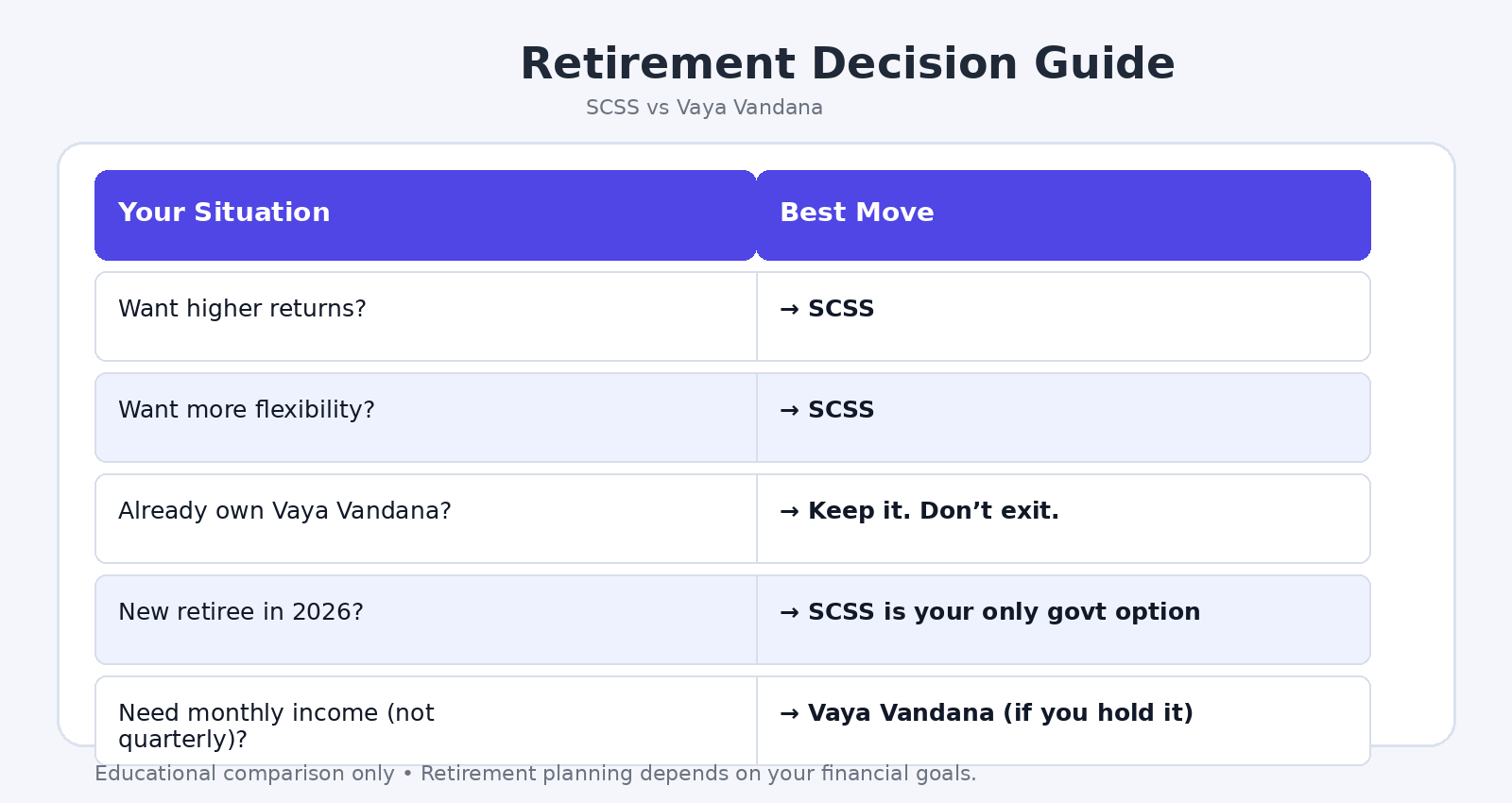

THREE REAL PEOPLE. THREE DIFFERENT ANSWERS.

Who Should Do What

The right answer depends entirely on where you are right now.

Rajesh — 60 years old, just retired with ₹50 lakhs

Best move: Open SCSS immediately.

Higher rate, shorter lock-in, tax benefit, and it's open right now. The decision practically makes itself. He gets ₹1,02,500 every quarter — no market-watching, no stress, no drama.

Priya — 65 years old, already holds Vaya Vandana (bought 2022)

Best move: Keep it. Don't exit.

She locked in a 10-year guaranteed income deal that nobody can buy anymore. The 2% early exit penalty makes leaving expensive. Her 'lower' rate is still a great deal, given what's available today.

Arjun — 58 years old, retiring in two years

Best move: Wait, then open SCSS at 60.

Vaya Vandana is permanently closed. SCSS is his only government-backed option. He should have documents ready so he can open the account the week he retires.

YOUR QUICK DECISION GUIDE

Match Your Situation

THE TAKEAWAY

The Smartest Decisions Are the Quiet Ones

Most retirement mistakes don't happen because people choose bad investments. They happen because people choose products they never fully understood.

SCSS versus Vaya Vandana was never really about 0.8%.

It was about lock-in flexibility when life throws surprises. It was about the inflation reality nobody puts in the brochure. It was about understanding that 'government-backed' and 'the best option available' aren't always the same sentence.

For most new retirees in 2026, SCSS quietly wins — not because it's exciting, but because it works. And for those already holding Vaya Vandana, the best move is to hold it with confidence.

Retirement should feel like a finish line. Not the starting gun for more confusion.

If this helped you — share it with the one person in your family who is still staring at those two brochures.

DISCLAIMER

This article is for educational purposes only and does not constitute investment or financial advice. SCSS interest rates are subject to quarterly revision by the Government of India. Vaya Vandana Yojana closure details are accurate as of the date of writing. All figures used are illustrative. Please verify current rates with your post office or bank before investing. Consult a SEBI-registered financial advisor for personalised guidance.

Disclaimer

What's Trending

Options Trading Explained with Pizza

April 1, 2026

IPO Buzz 2025: 3 Companies Investors Can’t Stop Talking About | GoPocket

September 25, 2025

New RBI Rules April 2026: What Changes for You

April 2, 2026

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.