Real Estate vs Stocks: The 10-Year Truth Most People Ignore

A senior Mumbai broker once told me he hadn't bought a second flat in 12 years. He sells them every week. His own savings? Index funds and SIPs. That single line changed how I think about Indian wealth-building.

Builders. Brokers. Property lawyers. The people who live and breathe Indian real estate often park their personal savings somewhere else entirely.

That raises a simple, uncomfortable question.

If property is the unbeatable investment your family insists it is, why do so many insiders prefer equity?

THE SHORT VERSION

Between 2016 and 2026, Indian equity index funds did most of the heavy lifting for patient investors. Real estate worked too, but hidden costs, home loan interest, and illiquidity ate a much larger chunk of returns than most people see on the surface. The right choice comes down to your goals, your time horizon, and how you behave when prices fall.

The Wealth Formula Most of Us Grew Up With

For two generations, the middle-class plan was simple. Buy a first home. Upgrade. Pick up a second flat as an "investment". Retire on rent and appreciation.

Property felt safe because you could touch it, visit it, and show it to your in-laws. Stocks felt abstract because they flash red numbers on your phone every single day.

But feeling safe and being efficient with your money are two different things. We confused one for the other for far too long.

Two Friends, Two Very Different Paths

Rahul buys a property. Puts down 20 per cent on a ₹1.5 crore flat in 2016. Twenty-year home loan. Feels proud. Family approves the same evening. Eventually finds a tenant.

Neha starts a SIP. Invests the same capital into a low-cost Nifty 50 index fund. Sets up an auto-debit and stops checking. No site visits. No tenants. No society WhatsApp groups.

Rahul's decision sounds responsible. Neha sounds boring. Boring, it turns out, has a strange habit of compounding into something serious.

Ten Years Later (2026)

The Part Property Ads Never Show You

Rahul's flat appreciated. That part is real. Over the same ten years, he also paid for a long list of things nobody mentioned at the showroom.

No single line item destroyed Rahul's returns. Together, they ate into them every year. That is why so many "great property investments" look very different once you do honest, full-cost accounting.

Meanwhile, Neha's Fund Just Compounded

No tenant calls. No leak in the kitchen ceiling. Just consistent investing and the simple math of compounding doing its work in the background.

The Nifty 50 has historically delivered around 13 to 14 per cent annualised over long-term ten-year stretches in India. Compounded across a decade of monthly SIPs, that builds a very different wealth picture than most people expect when they start with their first ₹5,000 instalment.

But Equity Is Not Emotionally Easy

In March 2020, the Nifty fell about 38 per cent in a few weeks. Many investors panicked, sold everything, stopped their SIPs, and locked in real losses. The ones who simply did nothing recovered fully within twelve months and went on to fresh highs.

The biggest risk in equity investing is rarely the market. It is your own behaviour when the market is bleeding.

Why Property Feels Safer Even When It Isn't

A stock market crash is visible the same minute it happens. A property correction is invisible for years.

If your flat drops 15 per cent in value, no one rings to tell you. There is no live ticker. So you go on believing your wealth is intact, even when it isn't.

Illiquidity hides volatility. It does not remove it.

Property's Real Superpower — Leverage

With a 20 per cent down payment, Rahul controlled a full ₹1.5 crore asset. When the property appreciated, the gain showed up on the entire value, not just his original cash. That is leverage, and it can multiply returns powerfully in a rising market.

It also magnifies losses, EMI stress, and bad-timing decisions. Leverage flatters you on the way up and punishes you on the way down. Most retail buyers only experience the second half of that sentence once.

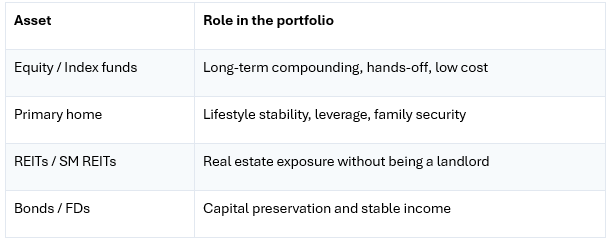

What Thoughtful Investors Actually Do

The smartest investors do not pick property or equity. They use both, in the right proportion, for different jobs.

Mutual funds Goal-based, diversified, professionally managed

This is exactly the structure GoPocket is built around. You can run a long-term equity SIP, build a mutual fund core for goal-based money, and as your wealth grows, step into bonds, REITs, ETFs and PMS — without juggling four different platforms or three brokers.

So Which One Actually Wins?

The honest answer depends on four things: your risk tolerance, your time horizon, how much liquidity you need at short notice, and whether you have the temperament to leave an investment alone for ten years.

But the bigger insight from the last decade is this. The investments that earn applause at family dinners are not always the ones building your real wealth. The ones building it are usually too boring to talk about.

A primary home you live in is a lifestyle decision, not an investment. A second flat bought purely as "investment" is exactly where most middle-class Indian wealth quietly went sideways. And a long-term equity SIP started in 2016 is exactly where the wealth showed up instead.

You do not have to choose a side in a war. You have to choose a portfolio.

Common Questions

Is real estate safer than stocks?

Not really. Property feels safer because its price does not flash red on your phone. But leverage and illiquidity create their own risks, which most retail buyers underestimate.

Why do so many Indians still prefer property?

Because it is tangible, emotionally grounding, and culturally validated. Touching the asset feels different from staring at a number in an app. That is a human response, not a financial one.

Can index funds beat property over 10 years?

Historically, broad-market Indian index funds have delivered stronger after-cost returns than most Tier-1 residential property over the 2016–2026 stretch, once you honestly account for stamp duty, interest, vacancy, and exit costs.

What is the biggest advantage of equity?

Liquidity, low cost, and built-in diversification. You can sell tomorrow if you need the money, your costs are tiny, and even a ₹5,000 SIP automatically spreads across 50 of India's largest companies.

Should I sell my flat and move everything to equity?

Not without thinking carefully. A primary home is partly a lifestyle asset. The argument here is against second flats bought purely as an investment, not against home ownership. Talk to a SEBI-registered advisor before any large reallocation.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Investments are subject to market risks. Past performance does not guarantee future returns. Please consult a SEBI-registered financial advisor before making investment decisions. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

What if your Daughter’s Dream-Wings Had a Price Tag? Secure Them Today!

September 25, 2025

Recent Blog

.jpeg)

.png)

.jpeg)

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.