Life Cycle Funds and Mutual Fund Gift Card (Gift PPI) 2026:

Rules, Dates and How They Work

SEBI introduced Life Cycle Funds — India's first target-date mutual funds — and proposed a mutual fund gift card (Gift PPI) in early 2026. Here's what both actually mean for Indian investors.

Quick Answer

In 2026, SEBI proposed Gift PPIs (mutual fund gift cards) — anyone can gift up to ₹50,000 for MF investing. It also introduced Life Cycle Funds, India's version of target-date funds, which automatically shift from equity to debt as your goal year gets closer. As of March 27, 2026: Gift PPIs are a proposal. Life Cycle Funds are approved and live.

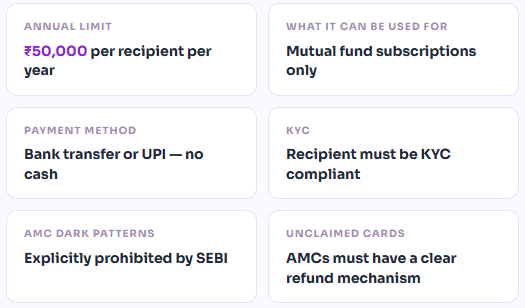

• Gift PPI (mutual fund gift card): SEBI consultation paper, March 25, 2026. Not live yet. Comments open until April 14, 2026. Limit: ₹50,000 per recipient per year.

• Life Cycle Funds: Approved via SEBI circular, February 26, 2026. Fixed maturity year, automatic glide path, no manual rebalancing needed.

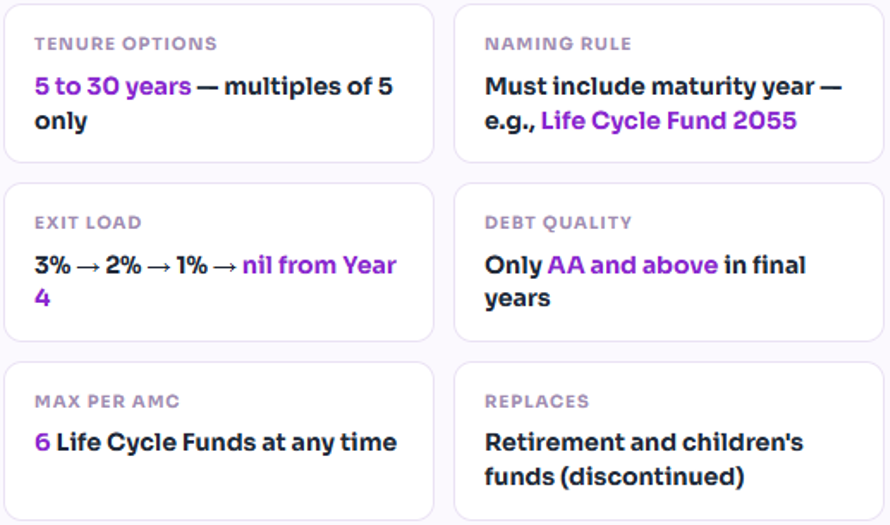

• Exit load: 3% in Year 1, 2% in Year 2, 1% in Year 3, nil from Year

• SEBI MF Regulations 2026 take full effect from April 1, 2026.

• Gift PPIs tackle the entry problem. Life Cycle Funds tackle the long-term management problem. They're designed to work together.

What is a Mutual Fund Gift PPI?

A Mutual Fund Gift PPI — Gift Prepaid Payment Instrument — is a proposed card that lets you buy up to ₹50,000 worth of mutual fund investment as a gift and hand it to someone else. They claim it, complete their KYC, and invest in whatever fund they choose on any AMC's website.

SEBI released the consultation paper on March 25, 2026. The idea came from AMFI. The stated goal is straightforward: getting first-time investors over the initiation hurdle by having someone else take the first step for them.

India has 26 crore mutual fund folios. Only about 8% of the population actually invests. That gap isn't a lack of awareness — most Indians have heard of mutual funds. The gap is the friction of starting: demat account, KYC, fund selection, and the anxiety of clicking invest for the first time. A gift card removes most of that friction from the recipient's side.

Proposal

As of March 27, 2026, this is a consultation paper — not a circular. SEBI accepts public comments until April 14, 2026. Terms and KYC requirements may change before the final notification.

How to use a Mutual Fund Gift PPI — step by step

1. Purchase the Gift PPI

Buy online or as a physical card through banking channels or UPI. Load any amount up to ₹50,000 per recipient per year. Cash transactions are not permitted.

2. Give it to the recipient.

Share digitally or hand over the physical card. Works for any occasion — birthday, Diwali, first salary, graduation. The card is locked to mutual fund investment only — it can't be used for anything else.

3. Recipient claims ownership

They register the card in their own name through the AMC website. KYC is mandatory before redemption. The investment goes in their name — not yours.

4. The recipient picks a fund and invests.

They choose any eligible scheme. Units are allotted at the applicable NAV. AMCs are explicitly prohibited from using dark patterns to nudge them toward any particular fund.

KEY RULES PROPOSED

Tax note: Gifts between close relatives — spouse, children, parents, siblings — are generally tax-exempt under the Income Tax Act. For non-relatives, gifts above ₹50,000 in a year may be treated as income in the recipient's hands. The proposed limit aligns with this threshold. Check with a tax advisor for your situation.

WHAT ARE SEBI LIFE CYCLE FUNDS?

Live

Life Cycle Funds are approved under SEBI circular dated February 26, 2026. Fund houses can launch schemes under this category now. SEBI MF Regulations 2026 take full effect from April 1, 2026.

A Life Cycle Fund is an open-ended mutual fund with a fixed target maturity year. It follows a predefined glide path — an automatic schedule that moves the portfolio from higher equity to higher debt as the maturity year approaches. You pick the fund once. It adjusts itself from there.

This is India's version of a target-date fund — standard in US retirement plans for decades. SEBI's framework brings a regulated form of the same idea to Indian mutual funds, with clear rules on naming, glide path bands, debt quality, and exit loads.

Life Cycle Funds replace the old solution-oriented schemes category (retirement funds and children's funds), which SEBI discontinued. The real difference: old solution-oriented schemes had goal-based names but no mandatory rebalancing over time. Life Cycle Funds have a date-linked glide path that is not optional.

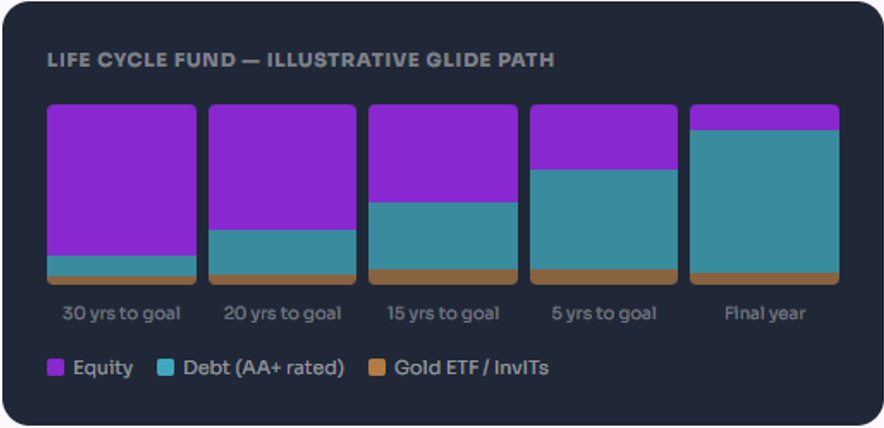

The glide path — how allocation shifts over time

Early in the fund's life, when the goal is 20–30 years away, equity can be 65–95%. As the maturity year closes in, equity reduces in stages and debt increases. In the final year, equity may be as low as 5–20%.

Example: Someone who buys a Life Cycle Fund 2055 in 2026 starts at roughly 80–90% equities. By 2045, the fund may be at 50–60% equity. By 2054, it's mostly high-quality debt. None of those shifts required any action from the investor.

The debt quality rule matters. In the final years of a Life Cycle Fund, all debt must be rated AA and above, with maturity dates no later than the fund's own target date. SEBI specifically closed the door on fund managers chasing yield through lower-quality bonds once the portfolio is shifting to a more conservative posture.

WHAT SEBI HAS SPECIFIED

GIFT PPI + LIFE CYCLE FUNDS: HOW THEY WORK TOGETHER

The two proposals target different problems. Gift PPIs handle the entry barrier — getting someone to start investing when they otherwise wouldn't. Life Cycle Funds handle the continuity problem — keeping investments appropriately managed over decades without requiring the investor to constantly make decisions.

ILLUSTRATIVE EXAMPLE

1. A relative buys a ₹10,000 Mutual Fund Gift PPI (once live) and gives it to a 25-year-old on their birthday.

2. The recipient completes KYC, claims the card on an AMC site, and puts it into a Life Cycle Fund 2060 — 34 years to their retirement goal. They also set up a monthly SIP.

3. The fund starts at high equity (80–90%). The investor gets on with their life.

4. Over the following decades, the fund automatically shifts toward AA-rated debt as 2060 approaches. No action needed.

5. Near 2060, the portfolio is predominantly stable debt instruments — protecting what was built over 34 years.

The bigger shift

Both proposals reflect SEBI's consistent push toward goal-based investing — where the product is designed around the investor's goal, rather than asking the investor to manually align a generic product to their needs. Life Cycle Funds are the clearest example of this in India's mutual fund space so far.

Risks and things to know before acting

Gift PPI — what to keep in mind

• Still a proposal. Final rules, implementation timelines, and KYC requirements are not confirmed. Don't count on it being live by a specific date.

• KYC must come first. The card is useless until the recipient completes KYC. If they haven't done it, factor in that lead time.

• Locked to MF subscriptions. It can't be redeemed as cash or used for anything other than a mutual fund investment.

• Not all AMCs may participate initially. Check with your preferred fund house once the mechanism goes live.

Life Cycle Funds — what to keep in mind

• No track record yet. This is a brand new category in India. No historical performance exists. Look at the AMC's broader reputation and the specific glide path design instead.

• Glide paths vary by AMC. SEBI sets bands, not exact numbers. Two Life Cycle Fund 2055 schemes from different fund houses may not hold identical portfolios at any given time.

• The exit load is real. 3% in Year 1 is significant. Don't invest in a Life Cycle Fund if there's any chance you'll need to exit within three years.

• Returns are market-linked. Shifting to debt reduces volatility — it doesn't remove risk entirely. The fund remains market-linked throughout.

• Goal year matters. If your goal changes substantially, the fund's glide path may no longer match your needs. You'd need to reassess.

GIFT PPI VS LIFE CYCLE FUNDS — SIDE BY SIDE

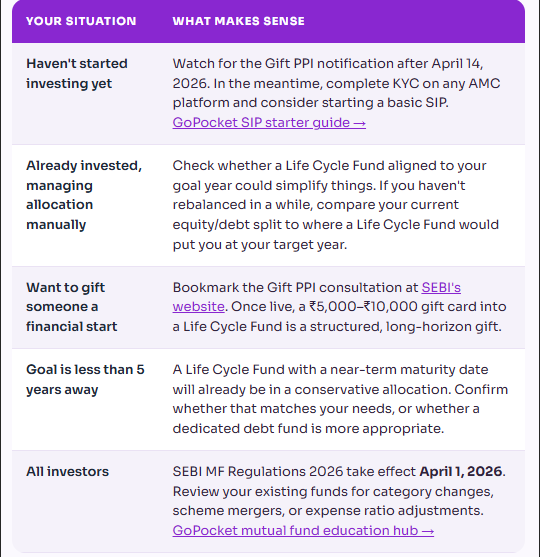

WHAT TO DO NEXT — BY INVESTOR TYPE

Disclaimer

This article is for informational purposes only and does not constitute financial, investment, or tax advice. The Mutual Fund Gift PPI is currently a proposal by the Securities and Exchange Board of India (SEBI) and is not yet implemented, while Life Cycle Funds are newly introduced and may vary across AMCs.

Mutual fund investments are subject to market risks. Please consult a qualified financial or tax advisor before making any investment decisions.

Disclaimer

What's Trending

How the Rich Use Loans Against Mutual Funds for Lifestyle

January 27, 2026

Top 5 Stocks in the Spotlight This Quarter: A Beginner's Guide

September 25, 2025

Expiry Day Thrills: How Thursdays Decide Millions in F&O | GoPocket

September 27, 2025

NSE F & O Explained: How Traders Earn in Just 2 Hours a Day | GoPocket

September 15, 2025

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.