THE BARBELL STRATEGY

Stop Playing It Safe in the Middle. That's Where Returns Go to Die.

Here's a question most financial advisors won't ask you:

"What if the safest-feeling investment is also the most dangerous one?"

Not dangerous because it'll blow up overnight. Dangerous because it quietly lets inflation eat your savings, your goals drift further away, and you spend years feeling financially "fine" — until you're not.

This is the trap of the middle. And the Barbell Strategy is built to get you out of it.

The Road Trip Nobody Wants to Take Twice

Imagine three people preparing for a long road trip.

Person A packs only safety gear — spare tyres, extra fuel, first-aid kits, backup kits for the kits. She never leaves the driveway.

Person B packs nothing but ambition. No spare. No emergency cash. One flat tyre, and the trip is over.

Person C carries one spare tyre, a first-aid kit, a charged phone — and then drives confidently toward the destination.

Person C isn't reckless. She isn't paralysed either. She's thought about what could go wrong and what needs to go right. That's the Barbell mindset in three characters.

What Actually Is the Barbell Strategy?

Nassim Nicholas Taleb — the guy who wrote The Black Swan and made "antifragile" a word people use at dinner parties — popularised this idea. The core insight is almost offensively simple:

Put serious weight on two ends. Ignore the mushy middle.

In investing, that means:

• One side of your portfolio is built for survival — stable, low-risk, sleeps well at night.

• The other side is built for upside — higher risk, higher potential reward, built for the long game.

• The middle? Skip it. Medium-risk, medium-return investments often give you the worst of both worlds.

It's not about being fearless. It's about being deliberate.

The Two Sides of the Barbell

🛡 Left Side: The Floor You Can Stand On

This side isn't meant to make you rich. It's meant to keep you in the game when things go sideways — and things always go sideways eventually.

Think of it as the seatbelt. You don't buy a car hoping to need the seatbelt. But you'd never drive without one.

What can go here:

• Emergency funds (3–6 months of expenses, non-negotiable)

• High-quality debt funds or bonds

• Fixed-income instruments

• Short-duration debt allocations

• Liquid assets you can access without panic

🚀 Right Side: Where Wealth Actually Gets Built

This is where you give your money a job with actual ambition. It will be volatile. It will sometimes feel terrible. That's the price of meaningful long-term growth — and because your safety side exists, you don't have to panic and sell at the worst moment.

What can go here:

• Equity mutual funds

• Index funds

• Large-cap and select mid-cap exposure

• Growth-oriented investments aligned to your timeline

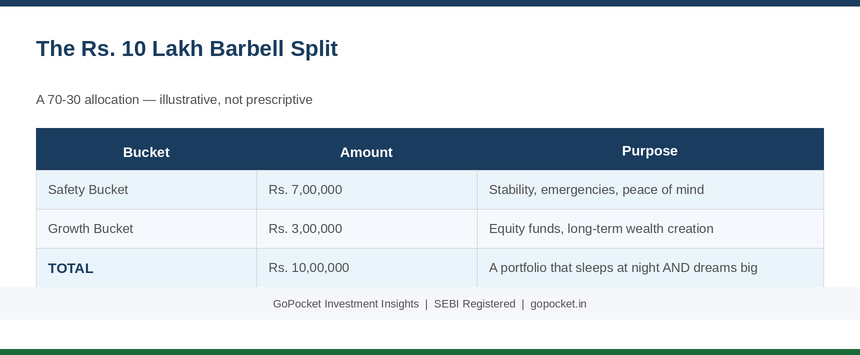

A ₹10 Lakh Example That Actually Makes Sense

Investor A puts everything into growth assets. High upside, sure — but one medical emergency or job loss, and they're forced to sell at the worst time.

Investor B uses the Barbell:

The ₹7L safety bucket means Investor B never has to make a desperate financial decision. The ₹3L growth bucket means they're still building wealth. The ratio isn't sacred — 80/20, 70/30, 60/40 all work. The principle is what matters.

Traditional vs. Barbell: The Honest Comparison

The Real Edge: Your Emotions

Here's what most investing content ignores — you're a human, not a spreadsheet.

When markets tank, investors without a safety cushion panic-sell at the bottom. When markets soar, investors sitting entirely in low-return assets feel left behind and chase hot tips at the top.

The Barbell strategy quietly solves both. You know your downside is protected. You know your upside is participating. That psychological clarity is worth more than any theoretical optimisation.

Discipline beats strategy. And the Barbell makes discipline easier.

5 Mistakes That Turn This Strategy Into a Mess

1. Calling everything a "Barbell"

Having 10 different mutual funds isn't a Barbell. Purposeful separation of safety and growth is.

2. Copying someone else's allocation

A 25-year-old and a 58-year-old should not have the same split. Context matters enormously.

3. Never rebalancing

If equities surge, your 70/30 might drift to 50/50 without you noticing. Review periodically.

4. Filling the growth side with hype

The growth side needs conviction and purpose, not whatever trend Reddit is excited about this week.

5. Expecting a guarantee

This is a framework for navigating uncertainty — not a promise of smooth sailing.

Is This For You?

The Barbell Strategy tends to click for people who:

• Want real growth without gambling their financial security

• Feel uncomfortable going fully aggressive — but know sitting fully in FDs isn't enough

• Have responsibilities (family, EMIs, goals) that mean they can't afford a total wipeout

• Want a framework they can explain to themselves at 2am during a market crash

It may not suit everyone. If you have very specific circumstances, age constraints, or income patterns, the implementation needs to reflect that. The concept is universal; the numbers are personal.

The Simplest Way to Remember This

Smart road trippers don't plan for perfect weather. They plan for the weather to change.

Carry the spare tyre. Keep enough fuel. Wear the seatbelt. Then drive confidently.

Successful investing isn't about choosing between safety and growth. It's about knowing how to use both — at the same time, on purpose.

The Barbell Strategy is one way to do exactly that.

Disclaimer

This blog is for educational purposes only and does not constitute investment advice. All market levels are approximate analyst estimates — not guaranteed outcomes. Past performance does not guarantee future results. Investments are subject to market risks. Please read all scheme-related documents carefully before investing. Consult a SEBI-registered financial advisor before making investment decisions. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

11 Best Sugar Stocks in India to Invest in 2024

May 21, 2024

The 4 Numbers That Move Every Market | GoPocket

July 31, 2026

Recent Blog

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.