The Mango Stand Secret: How Smart Traders Make Money Without Betting on the Market

Arjun was at Crawford Market last summer.

He spotted a vendor selling alphonso mangoes for ₹80 a kilo. Thirty steps away, another vendor — clearly unaware of the first — was asking ₹95 for the same thing.

Arjun quietly bought 10 kilos from the first guy and sold them to a nearby juice stall for ₹90. He made ₹100 in ten minutes without any mango expertise. No prediction. No speculation. Just a simple price gap, exploited cleanly.

That, in its most honest form, is arbitrage.

In financial markets, you're not moving mangoes. You're moving positions between the spot market (where you buy a stock or index today) and the futures market (where a contract locks in a price for a later date). And when those two prices drift apart more than your costs, there's money sitting there.

This blog explains two flavours of this — Cash & Carry and its mirror image, Reverse Cash & Carry. Both are used by institutional traders daily. Both are doable for retail investors who understand the mechanics.

Strategy 1: Cash & Carry Arbitrage — When Futures Are Overpriced

Let's say Nifty is at 22,000 in the spot market right now. But the one-month futures contract for the same Nifty is trading at 22,300.

That gap of 300 points exists. It didn't appear randomly — it usually reflects the 'cost of carry' (basically, the interest you'd pay to hold that position). But sometimes, the futures price overshoots. It gets more expensive than it should be.

That's your opening.

Here's what you actually do:

• Step 1: Buy Nifty in the spot market — say, via Nifty BeES (an ETF that tracks the index)

• Step 2: At the same time, sell an equivalent Nifty futures contract at the higher price

• Step 3: Hold both positions until the futures contract expires

• Step 4: Collect the difference — because at expiry, spot and futures always meet

Why do spot and futures prices converge at expiry? Because at expiry, the futures contract literally becomes the spot. If they didn't match, there'd be an instant arbitrage that would self-correct. Markets hate free money that's too obvious.

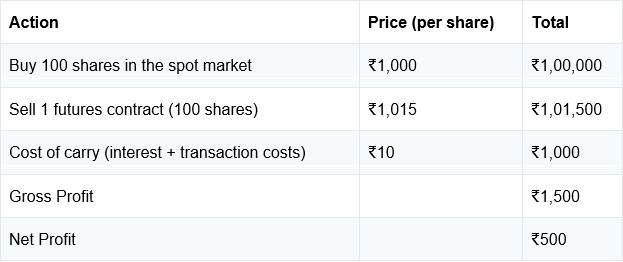

A Real Numbers Example

Let's make this concrete with 100 shares of a stock:

₹500 on ₹1 lakh deployed. That's a 0.5% return in one month, or roughly 6% annualised — without taking any directional view on whether the market goes up or down.

Not spectacular. But it's consistent, and it's not correlated to market direction. That's the point.

What is 'Cost of Carry' exactly?

Think of it as the price you pay for holding something. It includes:

• Interest — the financing cost on the ₹1 lakh you deployed in spot

• Brokerage — both legs (spot buy + futures sell)

• STT, exchange charges, GST, stamp duty

• Sometimes, dividend adjustment — if the stock pays a dividend before expiry, futures pricing reflects that

The arbitrage only works if the futures premium is bigger than all these costs combined. If the gap is too thin, you're not profiting — you're just paying fees.

Strategy 2: Reverse Cash & Carry — When Futures Are Underpriced

Same logic, flipped upside down.

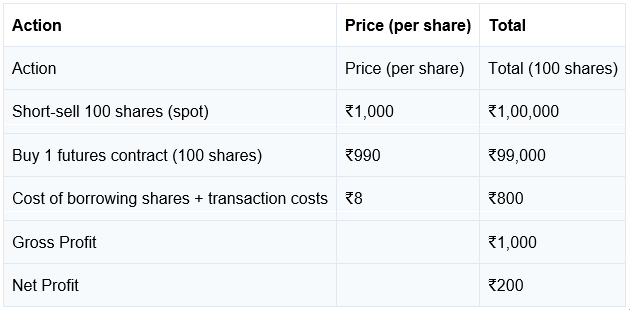

Imagine the same stock is at ₹1,000 in the spot market, but its futures are trading at ₹990. Futures are cheaper than the stock itself. That's called backwardation — it happens sometimes during dividend season or when there's heavy selling pressure in the futures segment.

The gap is ₹10. Your move? Do the reverse trade.

The steps:

• Step 1: Short-sell 100 shares in the spot market at ₹1,000 (you borrow shares, sell them, and get ₹1,00,000)

• Step 2: At the same time, buy 1 futures contract at ₹990

• Step 3: Hold until expiry — at which point both prices converge

• Step 4: Buy back the spot shares using the futures contract, pocket the difference

The numbers again:

₹200 on a ₹1 lakh trade. Smaller, but still real, and still market-neutral.

The hard part of Reverse Cash & Carry isn't the math — it's the short-selling. In India, the Securities Lending and Borrowing (SLB) mechanism exists for this, but liquidity is thin on most stocks. This is why this strategy is less common for retail investors than the regular Cash & Carry version.

What Can Go Wrong? (The Honest Part)

Every trading strategy sounds cleaner on paper than it is in real life. Here's what actually catches people:

1. You don't move fast enough

Arbitrage windows are narrow. Sometimes they're gone in seconds. Institutional desks run algorithms that spot these gaps the moment they appear. As a retail trader, you're not competing on pure speed — but you can look for larger, more persistent gaps that survive a few minutes.

2. The math changes mid-trade

If interest rates move sharply, or if the stock announces a surprise dividend, your cost of carry estimate goes off. You built your trade assuming ₹10 in costs; now it's ₹14. Suddenly, ₹15 gross profit becomes ₹1 net profit. Not worth the effort.

3. Margin requirements

You need to fund both legs. The spot position needs cash. The futures position needs margin. For Reverse Cash & Carry, you also need margin for the short-sell. Total capital requirement is always higher than the net profit looks. Factor this in before you start.

4. Liquidity isn't always there

If you're looking at a small-cap stock with thin futures trading, you may not be able to enter or exit at the prices you need. The spread between bid and ask eats your profit. Stick to Nifty, Bank Nifty, or large liquid stocks when you're starting.

5. SEBI rules keep changing

Short-selling regulations, F&O position limits, and margin requirements — these get updated. What's clean today might need a rethink next quarter. Staying updated is part of the job.

The GoPocket Angle

GoPocket gives you the infrastructure to actually execute this kind of trade — low brokerage on both cash and F&O segments, real-time data to spot gaps as they form, and the API access if you want to build a basic scanner yourself.

The reason most retail traders never attempt arbitrage isn't that it's too complex. It's that they never had a single platform where spot, futures, and all the cost data sat together clearly. That's what GoPocket is built for.

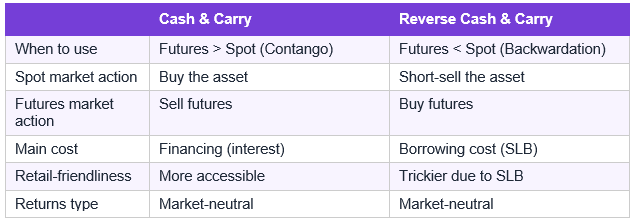

Quick Summary: Cash & Carry vs Reverse Cash & Carry

Before You Try This

A few things worth internalising:

• Never enter these trades without calculating your exact cost of carry upfront. The gross profit is visible; the net profit is what matters.

• Paper trade first. Run a few cycles on paper before you commit real capital. The mechanics are simple, but the execution discipline is different.

• Start with Nifty or Bank Nifty. They have the tightest spreads and deepest liquidity — which is exactly what arbitrage needs.

• These are convergence trades. They work because markets self-correct. Trust the mechanism, but monitor the position.

Arjun made ₹100 at Crawford Market. He didn't predict whether mango prices would rise next week. He just saw a gap, moved fast, and closed the loop.

That's all arbitrage is. The market version just has more zeroes.

Disclaimer:

Investments are subject to market risk. Please read all scheme-related documents carefully before investing. This blog is for educational purposes only and does not constitute investment advice.

Disclaimer

What's Trending

Equity vs. Shares: Understanding the Key Differences

January 5, 2024

Union Budget 2026–27 Decoded: Key Takeaways for Smart Investors

February 20, 2026

Recent Blog

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.