What Happens Next — Full Outlook: April 13–17, 2026

Nifty surged 6% last week — its biggest weekly gain in 5 years. But with crude oil edging toward $100, inflation data dropping today, and IT earnings kicking off midweek, the real question isn't how high we went. It's whether we can hold.

Quick Answer (TL;DR)

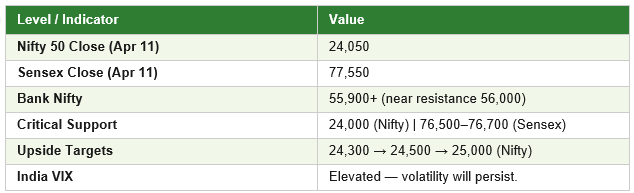

India's markets snapped a six-week losing streak with a near 6% weekly gain — Nifty closed at 24,050, Sensex at 77,550. Three things decide this week: CPI inflation data (today), US–Iran talks outcome, and Q4 FY26 earnings season.

As long as Nifty holds above 24,000, the mood stays cautiously bullish. A sustained break below signals the rally had no real conviction behind it.

Six Weeks. Then One Big Move.

Six weeks of selling pressure, six weeks of anxiety — and then last week, the market flipped. Nifty surged nearly 6%, Sensex crossed 77,500, short-sellers scrambled to cover, and FIIs returned as buyers. The shift was sharp and real.

But big bounces raise harder questions than big crashes. When markets fall, everyone asks, 'How low?' When they jump like this, the real question is: genuine recovery or just a sharp snapback in a still-shaky trend? This week, we find out.

The Setup: Key Levels That Actually Matter

Before diving into what to watch, here's a clean snapshot of where we stand heading into the week:

Note on F&O Expiry (Monday, April 13): Due to Tuesday's market holiday (Ambedkar Jayanti), this week's monthly F&O expiry was moved to today. That means heightened volatility in the morning session as traders close out derivative positions. If you see sharp swings early in the day, don't read too much into them. For long-term SIP investors, this changes absolutely nothing.

Three Events That Could Tip the Scale This Week

Here's what matters — explained simply.

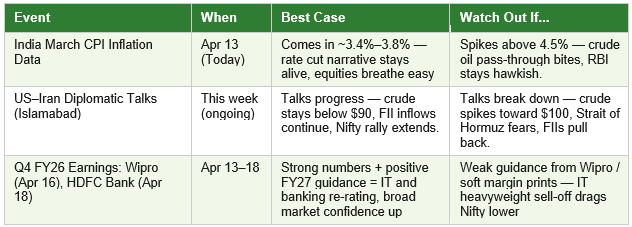

1. India March CPI Inflation — Out Today

India's retail CPI for March 2026 drops this afternoon. Economists polled by Mint expect it in the 3.1%–4% range, but with an upside bias — LPG prices rose ₹60 in early March, and energy costs from the West Asia conflict have seeped through partially.

February's print was 3.21%. A reading of 3.4%–3.8% keeps rate cut hopes alive. Anything above 4%–4.5% brings inflation concerns back, complicating the RBI's stance. Inflation shapes liquidity; liquidity drives valuations. This number matters.

2.US–Iran Diplomatic Talks — The Wildcard

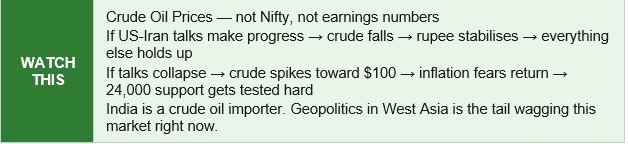

If one thing can override every other variable this week, it's this. The Islamabad talks ended last week without a concrete agreement; a follow-up round is underway. India imports ~87% of its crude oil, so every $5 rise costs an estimated $7–8 billion more annually — hitting the rupee, widening the current account deficit, and constraining RBI's ability to cut rates.

Shipping through the Strait of Hormuz is reportedly running at less than 10% of normal levels. Crude has eased since the April 8 ceasefire but remains well above pre-war levels. Progress in talks → crude falls → bullish for India. Breakdown → crude spikes toward $100 → 24,000 gets tested hard.

Watch crude prices as your leading indicator this week. Not Nifty. Not earnings. Everything else follows oil.

3. Q4 FY26 Earnings Season Gets Serious

TCS kicked off on April 9. The rest of the calendar:

• Wipro — April 16 (3:30–4:00 PM)

• HDFC Bank — April 18

• HCL Technologies — April 21

• Tech Mahindra — April 22

• Infosys — April 23

Markets react to guidance, not past numbers. For IT specifically, the Nifty IT index is now at ~17.8x one-year forward earnings — about 16% below its 10-year average and near pre-COVID valuations. The reset has happened; what the market needs is evidence that the worst is behind us. Wipro's Q1 FY27 guidance on April 16 is the number to watch.

Sector Spotlight: Where the Action Is

IT Stocks — Down 20%, Interesting Again

The Nifty IT index has corrected over 20% since January 2026, with valuations reset to pre-COVID levels — historically a good entry zone for patient investors. AI disruption concerns, slower deal ramp-ups, and cautious client spending drove the correction. But the haircut has been deep enough that even modest positive guidance on April 16 could trigger a sharp sector-wide recovery.

Banking — The Quiet Pillar

Bank Nifty closed above 55,900 last week, backed by strong fundamentals — HDFC Bank reported 15% deposit growth and 12% advance growth in its Q4 update. Full results drop on April 18. Key resistance sits at 56,300–56,500; support at 54,800–55,200. If the broader market wobbles this week, banking stocks will likely cushion the fall.

Energy — The Week's Dark Horse

Crude oil sensitivity means any positive development in Islamabad moves energy stocks fast. PSU oil companies deserve a spot on your watchlist this week, regardless of which direction talks go.

The Money Flow Picture

FIIs turned net buyers on Friday (April 11), adding ~₹672 crore. DIIs added ₹410 crore. But context matters: overseas investors have still net-sold ₹48,905 crore in April 2026 so far. One good session doesn't reverse weeks of outflows. Sustained FII buying across multiple sessions is the signal that gives this rally real legs.

The Global Context

US CPI came in at 3.3% for March, pushed by a 10.9% energy surge from the Iran war. Core inflation was tame at 2.6% — Fed officials are inclined to look past the energy spike. Markets are pricing minimal chance of a US rate cut for the rest of 2026.

A strong dollar pressures FII inflows into India. Asian markets are broadly lower in early Monday trade (Nikkei -1%, Hang Seng and KOSPI -1%+). Gift Nifty was down ~354 points in early morning — expect a cautious open today.

Market Internals: What Changed Last Week

The week's rally wasn't just an index-level event — it was broad-based, and that's important.

The honest read: last week shifted the short-term market structure from bearish to neutral-to-positive. It did not begin a new bull run. The bulls have a fighting chance — now they need to follow through.

The Psychology of This Market

We've moved from fear to hope. That's real progress. But hope is not yet confidence — and that gap is exactly why volatility stays high. Markets running on hope react badly to disappointment; any one of the three events this week going wrong can send Nifty back toward 23,500 fast.

This is a decision phase. The data will tell us whether the recovery has fundamental backing, or whether we just had a powerful bear-market bounce.

What Should You Actually Do?

Depends on where you are in your investment journey.

If you're a long-term SIP investor

Nothing changes. Not the CPI print, not the geopolitics, not the F&O expiry. Your SIP is built for exactly these uncertain periods — and the six-week correction followed by last week's bounce is a textbook example of why staying invested matters. Those who exited during the dip likely missed Friday's recovery.

If you have fresh cash to deploy

This is a higher-risk, higher-opportunity moment — the market has bounced hard but is still well below its January highs (Nifty peaked near 26,373). Stagger your investment over the next four to six weeks rather than going all in at once. Focus on large-cap fundamentals: banking and select IT names.

If you panicked during the correction

Reflect, don't rush. Timing exits is hard; timing re-entries is harder. If unsure, a conversation with a financial advisor is worth more than any headline right now.

The Single Most Important Thing to Track This Week

Final Market Outlook: April 13–17, 2026

Bias: Mildly bullish, with significant event risk on both sides. Expected Range: 23,800–24,600 (Nifty). A positive Iran talks resolution could push toward 25,000; a breakdown could retest 23,500.

This week is consequential — it will either confirm that India's equity market has found its footing, or reveal that last week was a powerful but hollow bounce. Stay watchful, stay disciplined, and don't let any single session override a well-considered long-term plan. Track inflation data, FII flows, and Q4 results in real time on GoPocket.

Disclaimer & Compliance

Investments are subject to market risk. Please read all scheme-related documents carefully before investing. This blog is for educational purposes only and does not constitute investment advice.

Disclaimer

What's Trending

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.