.jpeg)

Your Home Loan EMI Might Be About to Go Up.

For millions of people with home loans, this felt impossible just six months ago. Loan EMIs were actually falling. Life was getting a little easier. Then something changed — and this Friday, June 5, at 10 AM, the RBI (India's central bank) will tell us exactly how worried we should be.

Let's break this down simply — starting with the basics, then building up to exactly what could happen to your money.

First, let's understand who sets your interest rate

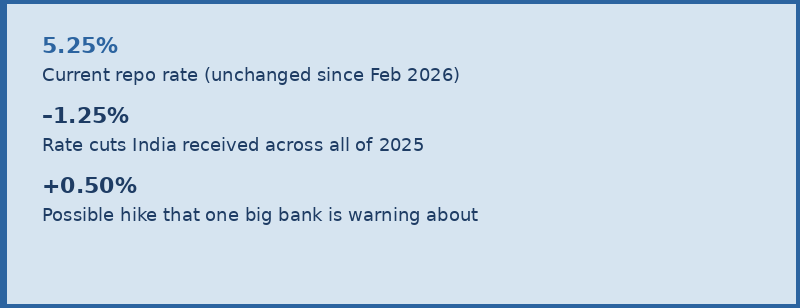

Think of the RBI (Reserve Bank of India) as the "bank for banks." All banks — SBI, HDFC, ICICI — borrow money from the RBI at a rate called the repo rate. Right now that rate is 5.25%.

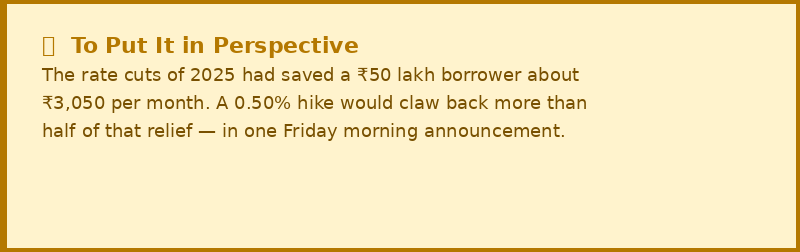

In all of 2025, the RBI cut this rate four times — a total drop of 1.25%. That's why EMIs were falling, and people were breathing easier. The question today is: is that chapter over?

The surprise forecast nobody is talking about

Almost every economist in India right now is saying the same thing: the RBI will keep rates the same on Friday. No change. Boring announcement. Go back to sleep.

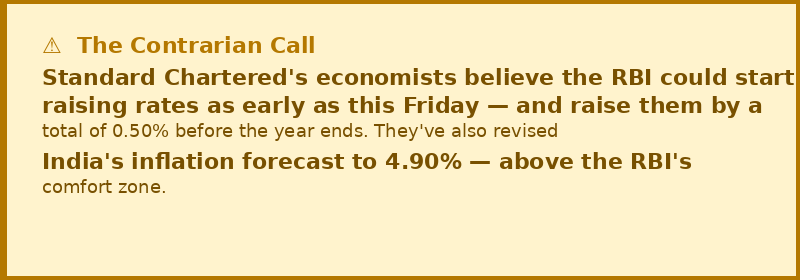

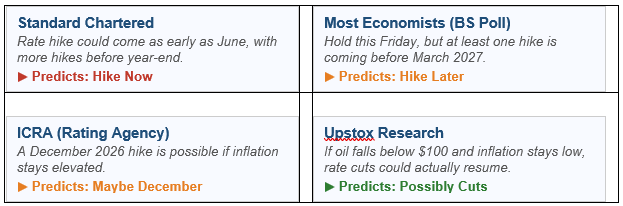

But Standard Chartered Bank — one of the biggest banks in the world — quietly published a very different prediction.

A 0.50% hike might sound tiny. But on a home loan, it adds up to serious money — every single month, for 20 years.

And Standard Chartered isn't alone. A Business Standard poll of economists found that while most expect no change this Friday, the majority believe at least one rate hike is coming before the year is out. The debate isn't if — it's when.

"Rising global interest rates and hikes by Indonesia and the Philippines may push India in the same direction."

— Outlook Money, May 2026

· · ·

Why is this even happening? 3 clear reasons

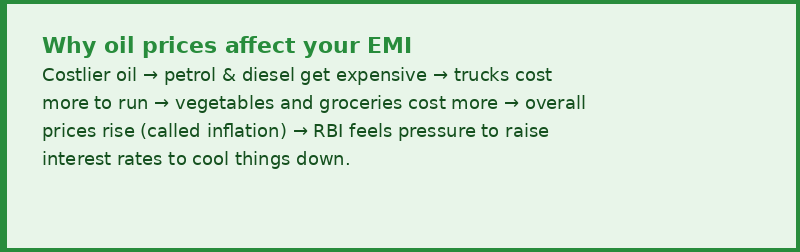

Reason 1 — Oil got expensive, and that breaks everything

The RBI built its whole inflation plan assuming oil would cost around $85 per barrel. In May, Brent crude crossed $100. That's because the ongoing West Asia conflict disrupted a major global oil supply route.

Reason 2 — The rupee weakened sharply.

The Indian rupee has fallen nearly 6% against the US dollar — touching near-record lows of ₹97 per dollar. This is a big deal because India buys oil in dollars. When the rupee weakens, oil imports cost even more in rupee terms — making the oil problem even worse.

Reason 3 — Fuel prices were already hiked

The government didn't wait — petrol and diesel prices were raised in May. Transport costs went up. Food delivery charges increased. Grocery bills quietly climbed. Economists call this the "domino effect" of inflation — one price rise triggers many others.

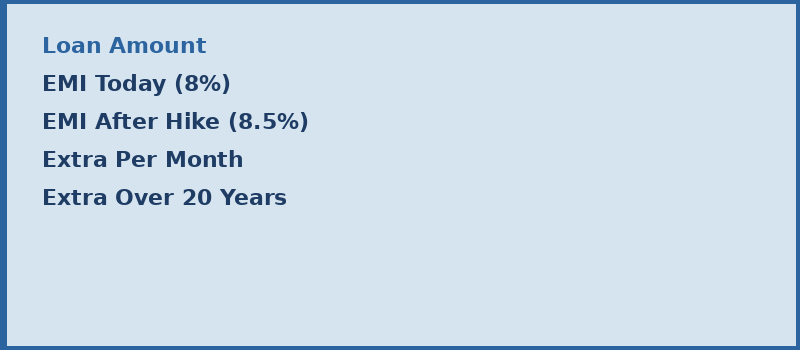

Okay — how much extra money are we actually talking?

Most home loans in India use a floating interest rate — meaning your EMI moves whenever the RBI moves rates, usually within 1 to 3 months of any announcement.

Here's the honest math. If the rate goes up by 0.50%, here's what happens to your monthly EMI on a 20-year loan:

Approximate figures for a 20-yearfloating rate home loan.

But here's the twist — the RBI might still hold

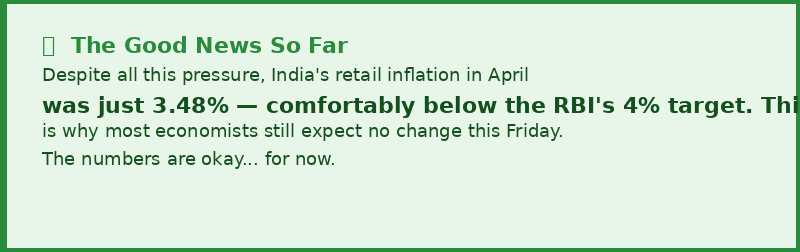

Remember that 3.48% inflation number? That's actually the RBI's best argument for doing nothing this Friday. Their job is to manage inflation — and inflation, right now, is still under control.

Here's where different experts actually stand:

Nobody knows for certain — not even the six people on the RBI committee who will vote on this. That uncertainty itself is the whole story.

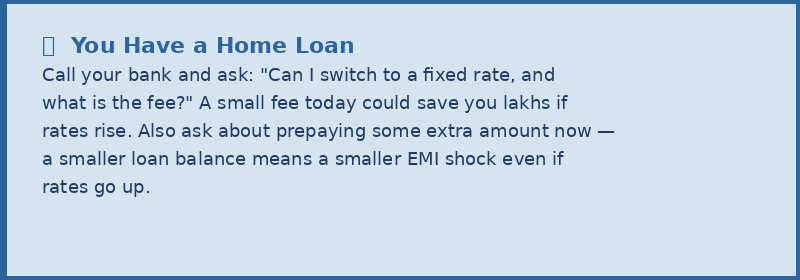

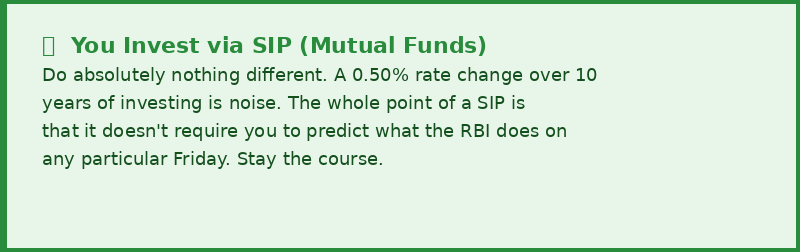

So what should you actually do?

Finally

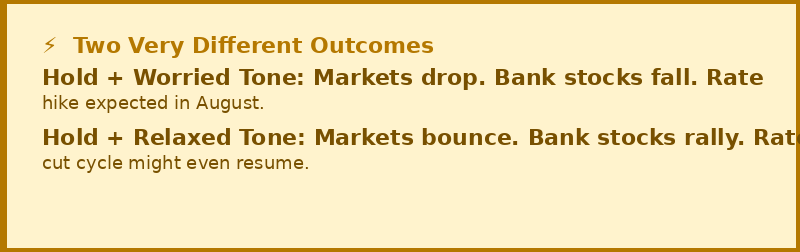

Even if nothing changes Friday — it still matters.

Here's what people miss: even if the RBI announces no change, the words Governor Sanjay Malhotra uses will move the markets.

The decision might be boring. The speech around it won't be. Set an alarm for 10 AM on Friday. That single press conference from one person in Mumbai will move billions of rupees — and possibly your monthly budget — in seconds.

That is what monetary policy looks like in real life. And now you know exactly how to understand it.

Disclaimer: This article is for educational purposes only and is not investment advice. EMI figures are approximate and for illustration only. All investments are subject to market risk. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

Netflix–WBD Deal Explained: Global Impact and India’s OTT Shift

December 20, 2025

Build Wealth in Your 20s: Simple Investing Guide for Indians

January 27, 2026

Recent Blog

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.