Imagine Getting a "Salary" Without the 9-to-5 Grind

The 2026 Guide to Your Monthly Post Office Paycheck.

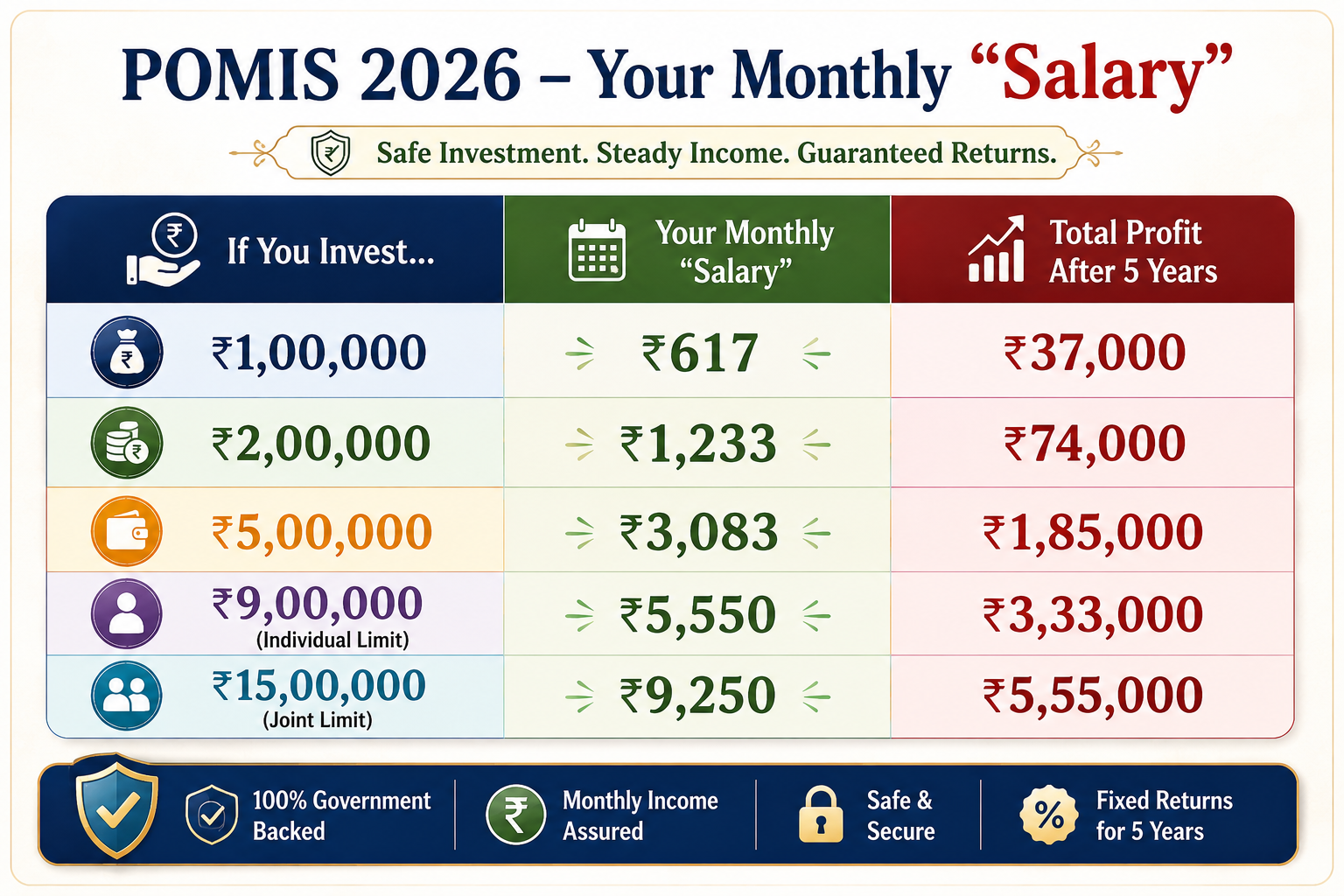

Ever had that dream where you wake up on the first of the month, check your phone, and see a notification that says: “₹9,250 has been credited to your account”?

Now, imagine that happening without a boss to answer to, no deadlines to chase, and—this is the best part—absolutely zero risk of losing your money.

For most, this sounds like a retirement fantasy or a lucky break. But for millions of smart Indian families, it’s just a regular Tuesday. They’re using the Post Office Monthly Income Scheme (POMIS) to build a life where their money does the heavy lifting.

In a world where crypto crashes make headlines and the stock market feels like a roller coaster, POMIS is like that reliable "grandfather" of investments. It’s steady, it’s calm, and it’s backed by the strongest guarantee in the country: the Government of India.

Whether you're a young professional looking to cover your monthly EMIs, a parent setting up a "future fund" for your kids, or you want to make sure your parents are financially independent, this 2026 guide is for you.

1. So, What Exactly is POMIS? (Think of it as your "Pocket Money" Fund)

Forget the boring financial definitions. Think of POMIS as a high-tech, government-backed piggy bank.

Here’s the deal: You "park" a lump sum of money with the Post Office for 5 years. In exchange for letting the government use that money to build things like schools and highways, they send you a "thank you" payment every single month.

After 5 years, they hand you back every single rupee you started with. It’s that simple.

Why is everyone talking about it in 2026?

While everyone else is chasing "get rich quick" schemes on social media, smart investors are sticking to POMIS because:

• 7.4% Interest: That’s way better than what your regular savings account is giving you.

• Sleep-at-Night Safety: Your money isn't tied to some risky startup. It’s a direct promise from the Indian Government. As long as the Post Office exists (and it’s been around for 160+ years), your money is safe.

• Total Automation: Once it’s set up, the money just appears in your account. No charts to watch, no news to follow.

2. The "Monthly Salary" Calculator: What’s Your Number?

The best thing about POMIS is that there are no surprises. You know exactly what’s coming. The current 2026 rate is 7.4% per year, split into 12 monthly instalments.

Here’s a quick breakdown of what your "monthly salary" could look like:

Note: You can start with as little as ₹1,000!

The "Joint Account" Pro-Tip

Notice the jump from ₹9 Lakh to ₹15 Lakh? If you open an account alone, the government caps you at ₹9 Lakh. But if you open a Joint Account with your spouse or parent, that limit shoots up to ₹15 Lakh.

For a couple, that’s a combined monthly income of ₹9,250—enough to cover the groceries, the electricity bill, or even a good chunk of a child’s school fees!

The "Joint Account" Pro-Tip

Notice the jump from ₹9 Lakh to ₹15 Lakh? If you open an account alone, the government caps you at ₹9 Lakh. But if you open a Joint Account with your spouse or parent, that limit shoots up to ₹15 Lakh.

For a couple, that’s a combined monthly income of ₹9,250—enough to cover the groceries, the electricity bill, or even a good chunk of a child’s school fees!

3. POMIS vs. Bank FDs: Who Wins the Battle?

Most of us default to Bank Fixed Deposits (FDs) because they’re familiar. But POMIS often has the upper hand. Here’s why:

• Payout Frequency: Most FDs pay you at the very end. POMIS is built for the monthly cash flow. If you have bills to pay now, POMIS is your winner.

• The "Sovereign" Shield: While big banks are safe, POMIS is a Sovereign Guarantee scheme. This means the Government of India itself is the borrower. It’s the highest level of safety you can get.

• The Tax Perk: The money you put in (up to ₹1.5 Lakh) can help you save tax under Section 80C. Many regular FDs don't offer this unless you lock your money for 5 years at a lower interest rate.

4. Is This the Right Move for You?

At GoPocket, we don't believe in "one size fits all." Here’s the truth:

It’s a PERFECT match if:

• You’re a Retiree: You’ve worked hard for decades; it’s time your money did the same. POMIS gives you that steady, pension-like feeling.

• You Hate Risk: If seeing your bank balance dip even by ₹1 makes you lose sleep, POMIS is your financial security blanket.

• You Have a Fixed Monthly Bill: Got a ₹5,000 EMI? Park ₹9 Lakh in POMIS and let the investment pay it for you!

It might NOT be for you if:

• You’re in your 20s and want to build a fortune: 7.4% is great for safety, but it won't make you the next billionaire. If you have time on your side, Mutual Funds or SIPs (check the GoPocket app!) are better for long-term growth.

• You Need the Money Next Month: This is a 5-year commitment. If you need quick cash, look at Liquid Funds instead.

5. The "GoPocket" Strategy: The POMIS-SIP Combo

Want to know how the real pros play the game? They don't just spend the interest on snacks. They use a strategy we call "Double Compounding."

How it works:

1.Invest ₹15 Lakh in a Joint POMIS account.

2.Get that ₹9,250 every month.

3.Immediately put that same ₹9,250 into a SIP (Systematic Investment Plan) in the stock market.

The Result: Your "Seed" (the ₹15 Lakh) is 100% safe with the Government, but you’re using the "Fruit" (the interest) to grow aggressively in the market. It’s the ultimate way to build wealth without ever risking your core savings!

6. The "Honest Truth"(The Stuff They Hide in the Fine Print)

We promised no jargon, so here’s the reality check:

• The 5-Year Lock-in: You’re "married" to this for 5 years. If you want a "divorce" (withdraw) early:

◦ Between 1-3 years: They’ll cut 2% from your money.

◦ After 3 years: They’ll cut 1%.

◦ Rule of thumb: Only invest money you don't need for the next 5 years.

• Tax on the Interest: While the investment saves tax, the monthly "salary" you get is taxable. It gets added to your income, and the taxman will want his share.

• The Inflation Trap: 7.4% is fixed. If the price of milk and petrol goes up by 8% next year, your money’s "buying power" might feel a bit weaker. (This is why the POMIS-SIP combo is so smart!)

7. How to Get Started in 3 Easy Steps

Opening a POMIS account is a bit "old school," but it’s easy:

1. The Kit: Grab your Aadhaar, PAN card, and 2 passport photos.

2. The "Lal Dabba: Head to your nearest Post Office and ask for "Form A".

3. The Deposit: Pay by cheque (it’s safer and easier). Once it clears, you’re in!

Pro-Tip: Ask the postmaster to link the payments directly to your regular bank account. That way, you don't have to visit the post office every month to collect your cash!

The Final Verdict: "Go" or "No"?

The Post Office Monthly Income Scheme is the ultimate financial security blanket. It’s warm, it’s safe, and it’s comfortable.

In 2026, as we see more "get rich quick" apps failing, the humble Post Office reminds us that consistency is the true secret to wealth. If you want a guaranteed, stress-free monthly income that lets you sleep like a baby, POMIS is a resounding "GO!"

Just don't let it be your only investment. Use it as your solid foundation, then use the

Ready to start your journey? Head to your local Post Office today!

Disclaimer: All rates and rules are as per the latest 2026 government guidelines. GoPocket is a SEBI-registered intermediary here to make your financial journey simple, safe, and successful

Disclaimer

What's Trending

Why Children Deserve to Learn ‘Money-Lessons’ in School | Gopocket

September 9, 2025

Every Candle Tells a Story – But Only Few Can Read It

December 10, 2025

Recent Blog

.jpeg)

.jpeg)

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.