Indian Markets: Week Ahead

April 28 – May 1, 2026

Simple. Honest. Practical.

Important: Markets are open Monday to Thursday only. Friday (May 1) is Maharashtra Day. Four sessions. A lot is riding on them.

WHAT HAPPENED LAST WEEK

Worst week in months. Three straight days of selling, zero recovery. Four things broke at once.

Oil spiked. Brent crude briefly crossed $100/barrel before settling at $94–98. The US–Iran conflict is choking the Strait of Hormuz — the channel through which 20% of the world’s oil flows. India imports 85% of its crude. Every $5 rise in oil hits petrol, diesel, transport, and manufacturing costs — and weakens the rupee.

The rupee slipped. Fell to ₹93–94 per dollar, swinging in a ₹92.25–94.62 range — unusually wide. When the rupee weakens, imports get costlier, and foreign investors earn less on their Indian bets.

FIIs kept selling. Foreign funds have pulled ₹1.75 lakh crore (~$21 billion) out of India in 2026. ₹44,000 crore left in April alone. Domestic funds (DIIs) tried to absorb it — buying ₹9,782 crore during the week — but by Friday, even they turned sellers. Both sides let go of the rope at once.

The RBI flagged a slowdown. Softer consumer spending. Slower bank lending. Not a recession — but the pace of growth is cooling.

HOW THE MARKET ACTUALLY FEELS RIGHT NOW

Three numbers tell the real story beneath the headlines.

India VIX: 19.71 — This is the market’s fear gauge. Normal range is 12–20. At 19.71 and rising (+6% on the day), investors are nervous but not panicking. If it crosses 25 this week, expect wild intraday swings. For context: it hit 86 during COVID.

Nifty P/E: 20.85 — How much are you paying for every rupee of earnings? At 20.85, the market is right at its long-term average of 20–21. Not a screaming buy, not dangerously expensive. The COVID crash took it to 17. The frothy peak hit 32. Right now, we’re in the middle — fairly valued.

India Manufacturing PMI: 55.9 — Above 50 = growth. This is the number the headlines are ignoring. India’s factories are doing well. April’s reading jumped from 53.9 in March. New orders up, employment hit a 10-month high, export orders grew at their fastest in nine months. The real economy is holding up better than the stock market suggests.

INDIA’S KEY NUMBERS AT A GLANCE

One connection worth understanding: The gap between US yields (4.31%) and Indian yields (~6.95%) — about 264 basis points — is what foreign investors watch. When US yields rise, that gap narrows, and India becomes less attractive. That’s exactly why the Fed meeting this week matters so much for us.

THE RETAIL INVESTOR’S SILVER LINING

While FIIs are selling, Indian retail investors are doing the opposite — quietly and consistently.

March 2026 AMFI data:

• SIP contributions hit a record ₹32,087 crore — up 7.5% from February

• Equity mutual fund inflows reached ₹40,450 crore — a 56% jump, the highest since July 2025

• This is the 61st consecutive month of positive equity fund inflows

• 9.72 crore SIP accounts were active as of March 31, 2026

The MF industry’s AUM dropped from ₹82 lakh crore to ₹73.73 lakh crore — but that’s just market prices falling, not investors running. One in every five rupees in the mutual fund industry now comes from SIPs. Retail India is quietly buying the dip.

THIS WEEK’S SCHEDULE

Monday, Apr 27:

Bajaj Finserv Q4 results. US Fed meeting begins. Sapphire Foods, Unicommerce, and Websol Energy also report.

Tuesday, Apr 28:

Vardhman Special Steels & Zenotech Labs results. Citius Transnet InvIT likely listing.

Wednesday, Apr 29:

Adisoft Technologies listing (NSE SME). US Fed decision + Powell press conference. US Q1 GDP advance estimate release.

Thursday, Apr 30:

Markets open (normal trading day).

Friday, May 1:

Markets closed — Maharashtra Day.

THE 5 THINGS THAT WILL MOVE MARKETS

1. Bajaj Finserv Q4 (Monday) Analysts expect ₹2,300–2,500 crore net profit on ₹33,000–35,000 crore revenue. Financials are the Nifty’s largest sector. A beat = shot at reclaiming 24,000. A miss = the index loses its most important pillar. This single result sets the tone for the entire week.

2. US Fed Meeting (Wednesday presser) Rate hold at 3.50–3.75% is 97.9% priced in. Nobody cares about the decision. Everyone cares about what Powell says. Markets see only a 14–38% chance of a June cut. Over half of Reuters-surveyed economists expect no cut through September. Nearly a third expect no cuts at all in 2026. Hawkish Powell = more FII selling. Dovish Powell = relief rally.

3. US Q1 GDP (Wednesday, 6 PM IST) Flying under the radar in India, but it shouldn’t be. The Atlanta Fed’s model puts US Q1 growth at just 1.2% annualized — down from an initial 3.1% estimate. US Q4 2025 already came in at a soft 0.5%. A weak number puts more pressure on the Fed to cut (positive for India). A stronger number reinforces ‘no cuts in 2026’ (negative).

4. Over 200 Earnings (All week) Nifty IT is already down 16.9% YTD after weak guidance from Infosys and HCL. If financials falter after Bajaj Finserv, the market loses two of its biggest pillars at the same time. Tuesday’s Zenotech (pharma) and Vardhman (steel) add sector-level colour.

5. Oil and FII Flows (Daily watch) Brent at $94–$100/barrel with the Strait of Hormuz partially blocked. Ceasefire holds → oil eases to $85–90 → rupee stabilises → FII selling slows. Ceasefire breaks → oil spikes to $120–150 → everything gets worse for India.

KEY MARKET LEVELS

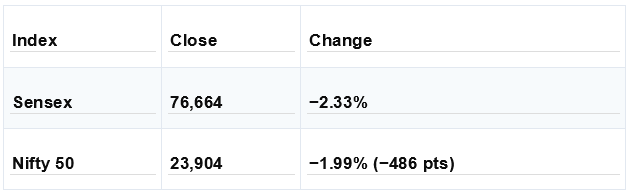

Nifty 50 (closed at 23,904):

• 24,000–24,200 → First resistance. Cross this, and recovery begins.

• 23,650 → First support. Near the 50-day moving average.

Bank Nifty (near 50,000): Monday’s Bajaj Finserv result is the sole swing factor.

• Beat → Rally toward 50,650–51,400

• Miss → Likely break below 50,000

IPO CORNER

Adisoft Technologies (NSE SME): Allotment Apr 28, listing Apr 30. Band: ₹163–172, lot size 800 shares.

Amba Auto Sales (NSE SME): Subscription Apr 27–29. Band: ₹130–135.

Citius Transnet InvIT (NSE SME): Tentative listing Apr 29. Infrastructure trust.

Note: Grey Market Premium (GMP) figures on social media are sentiment indicators only — not reliable predictors of listing price.

WHAT THIS MEANS FOR YOU

Running a SIP? Don’t touch it. Keep it going.

SIPs are built exactly for weeks like this. When prices fall, your monthly amount quietly buys more units — that’s the whole magic. A 2% dip isn’t a warning sign; it’s your SIP doing its job. The worst thing you can do right now is stop it.

Here’s a number to hold onto: ₹10,000 a month in a simple Nifty 50 index fund over the last 10 years would have grown at roughly 12–14% a year — through COVID, multiple market crashes, global slowdowns, and dozens of weeks scarier than this one.

Have cash sitting on the side? Don’t dump it all in at once.

Too much is happening at the same time — the US Fed decision, Bajaj Finserv results, oil prices swinging, and a shortened trading week. Any one of these could jolt the market either way.

The smarter move: wait for Wednesday’s market close. Once the Fed speaks and the US GDP number drops, you’ll have a much clearer picture of where things are heading. Then invest in 3 or 4 smaller chunks spread over the next 2–3 weeks, rather than going all-in at one point.

Trading in futures same.or options? This week needs extra caution

Two things to keep in mind.

First, Friday is a holiday, but options don’t take a day off. Time decay (theta) — the gradual loss in an option’s value simply due to the passage of time — continues even when markets are closed.

You’ll come back on Monday with positions worth less, even if nothing else has changed.

Second, a four-day trading week with multiple major events means:

• Thinner liquidity

• Wider bid–ask spreads

• Sharper, sometimes unpredictable price moves

Experienced traders usually reduce position sizes ahead of long weekends. It’s a sensible approach to consider this week as well.

THE GOLDEN RULE FOR THIS WEEK

Watch the closing prices. Ignore the intraday noise.

Monday and Tuesday will have plenty of dramatic moves — up, down, sharp, sudden. Most of it will reverse or mean nothing by the end of the day. The closing price on Wednesday, after the Fed and the US GDP data are both out, is the number that actually tells you where the market is going next. That’s the one to pay attention to.

Stay calm. The fundamentals — 7.6% GDP, 55.9 PMI, record SIP inflows — haven’t broken. The market is nervous. That’s different from the economy being broken.

Data as of April 25–27, 2026. For information only — not investment advice.

Disclaimer

What's Trending

What Makes Silver Prices Move & How to Invest Wisely

January 23, 2026

How to Start SIP Investment Online in 5 Simple Steps

October 28, 2025

The Habit That’s Secretly Eating Your Wealth

August 7, 2025

Indian Market Rebounds: GoPocket's Weekly Ups & Downs

April 20, 2026

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.