.jpeg)

SIP vs Lump Sum: Which Strategy Wins in a Volatile Market?

The real debate isn't about strategies — it's about staying invested when markets get uncomfortable.

Rohan andVikram had the same goal, the same mutual fund, and the same Rs. 6 lakh to investpayout and. Then the market turned volatile — and everything changed.

One received his money as a maturity payoutand put it all in at once. The other planned to invest gradually through a SIP. Same fund, same starting point — but two very different journeys. And when the market began swinging, both found themselves asking the same question millions of investors ask every year:

"Should I invest everything at once, or should I drip it in through SIP?"

It sounds simple. But behind it lies one of the most paralysing dilemmas in retail investing — one that causes many people to delay investing altogether while waiting for the "right" answer.

The Real Problem Isn't the Strategy

Here's what most comparison articles won't tell you: the biggest threat to your wealth isn't choosing SIP over lump sum. It's waiting too long to decide at all. Think of someone standing at a railway station who knows their destination but can't decide which coach to board. They keep analysing. And the train leaves.

Markets rarely offer perfect clarity. That's not a flaw in the system — it's simply how markets work. The sooner investors accept this, the sooner they can stop waiting and start participating.

What SIP Actually Does for You

Rohan's SIP meant he invested a fixed amount every month, regardless of market conditions. Some months he bought at high prices. Some months at lower ones. But he always bought — and that consistency is where the real value lies.

Over time, this averages out the cost of purchase — a mechanism widely known as Rupee Cost Averaging. More importantly, it removes the pressure of timing the market perfectly. Investing becomes a habit rather than a high-stakes monthly decision.

In volatile markets especially, SIP offers something money can't buy directly: emotional comfort. When you're not betting everything on a single day's price, drawdowns hurt less. And investors who aren't emotionally rattled are far more likely to stay invested.

Why Lump Sum Isn't the Reckless Choice It Sounds Like

Vikram's lump sum investment came with immediate nerves. What if the market drops tomorrow? What if this is the worst possible time to invest? These concerns are valid — but they have a flip side.

A lump sum puts your entire capital to work from day one. If markets trend upward over the long term (as they historically have), every rupee benefits from compounding for the maximum amount of time.

This is exactly why investors who receive bonuses, inheritance proceeds, or large one-time payouts often opt for lump sum investing. Keeping money parked in a savings account while waiting for the "right" moment is itself a financial decision — and not necessarily a wise one.

The Myth of Perfect Market Timing

The real reason people resist lump sum investing is the belief that they can identify the ideal market entry point. Let's be direct: almost no one can do this consistently — not even seasoned fund managers.

Markets respond to earnings, interest rates, global events, policy changes, and a thousand factors no model can fully predict. Trying to outsmart every one of them is a pursuit that has cost more investors more money than any single wrong investment decision.

The investor who waits for certainty doesn't lose money. But they also don't build wealth.

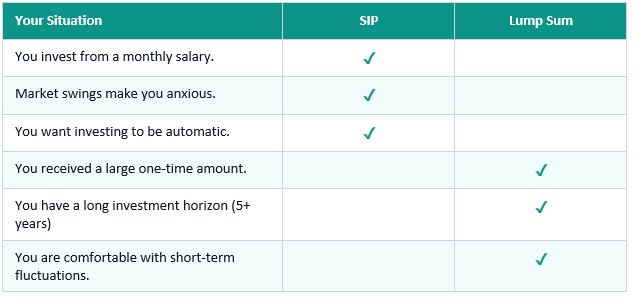

SIP or Lump Sum? A Practical Guide

Rather than declaring a winner, here's a straightforward way to think about which fits your situation:

Notice that neither column is objectively superior. They serve different investors in different situations. And for many people, a combination of SIP + lump sum — investing a lump sum now while continuing a SIP from monthly income — is the most practical path.

The Hidden Cost of Doing Nothing

There's a mistake many investors make that doesn't show up in any comparison chart. They spend months researching SIP vs lump sum. They watch videos, read articles, monitor markets — and then do nothing.

A decent strategy started today almost always outperforms a perfect strategy started next year. Compounding rewards participation, not deliberation.

KEY INSIGHT: The most expensive investment decision is often the one you never make. Every month of delay is a month of compounding your money you never got.

Behaviour Matters More Than Strategy

Here's the part most comparison articles skip: neither SIP nor lump sum works if the investor doesn't stay the course.

An investor who starts a SIP but pauses it every time markets dip will underperform. An investor who makes a lump sum investment and sells at the first sign of volatility will also underperform. Strategy is just the starting point. Discipline is what converts strategy into wealth.

Rohan and Vikram both came to understand this over time. The market rose and fell, surprised them more than once, and tested their conviction. What ultimately mattered was that they stayed invested — and stayed committed to their original reasoning.

The Better Questions to Ask

Instead of asking which strategy wins, ask yourself these:

→ How much money do I have available to invest right now?

→ What is my — months, or years? investment horizon

→ How will I feel if the market drops 20% next month?

→ Will I stay invested during a prolonged downturn

→ What approach makes me more likely to remain disciplined

These questions don't have universal answers — but they have your answer. And that's the only one that matters.

So, Which Strategy Actually Wins?

The honest answer: it depends — but the more important answer is that the debate itself is a distraction. Both SIP and lump sum, used appropriately, have helped investors build real wealth over time.

The winner in volatile markets isn't the strategy. It's the investor who takes a considered decision, doesn't panic when conditions change, and stays committed to a long-term plan. Because in investing, consistency almost always matters more than perfection.

Disclaimer

What's Trending

Don’t let party nights steal your future: equities show the smarter way

September 16, 2025

Recent Blog

Blog

Recent Blogs

.jpeg)

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.