LARGE CAP VS MID CAP VS SMALL CAP FUNDS: THE HONEST COMPARISON

The day three investors looked at the same market… and saw three completely different worlds.

It was a normal weekday morning. Same market. Same Nifty chart. Same news headlines shouting about inflation, interest rates, and global uncertainty. But inside a small office in Chennai, three investors were reacting in three completely different ways.

Ravi, a 45-year-old government employee, smiled calmly. His large-cap portfolio was slightly green. Nothing exciting, nothing dramatic. Just steady.

Meena, a 32-year-old entrepreneur, kept refreshing her mid-cap fund. It was swinging up 1%, down 2%, then again up. She felt both anxious and thrilled at the same time.

Arjun, a 26-year-old first-job engineer, was watching his small-cap investment like a thriller movie. It was either “wow” or “why did I even invest?” nothing in between.

Same market. Three completely different emotional experiences. And here’s the uncomfortable truth nobody tells beginners:

You are not choosing a fund category. You are choosing your emotional tolerance for chaos disguised as wealth creation. That’s what Large Cap vs Mid Cap vs Small Cap really is.

Not finance. Behaviour.

WHY YOUR BRAIN IS SECRETLY BIASED TOWARD ONE CATEGORY (EVEN BEFORE YOU INVEST)

Most investors believe they are logical. They say things like “I want good returns with safety.” But markets don’t reward intentions. They reward behaviour.

• Large caps feel safe because they are familiar names. Your brain trusts familiarity more than numbers.

• Mid caps feel exciting because they move faster. Your brain mistakes motion for opportunity.

• Small caps feel like lottery tickets because they are unknown stories waiting to explode.

This is where most investors unknowingly make their first mistake: They don’t pick based on goals. They pick based on emotions.

Most investors don’t lose money because of bad stocks or funds. They lose money because they switch categories at the wrong emotional time.

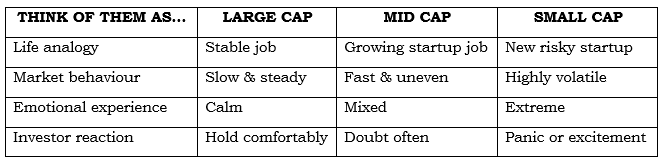

THE HIDDEN PERSONALITIES BEHIND EACH MARKET CAP

Think of them like three characters in a movie:

Large Cap = The experienced elder

Stable, predictable, doesn’t panic easily, but doesn’t surprise you often.

Mid Cap = The ambitious climber

Not fully stable, not fully risky, constantly trying to prove itself.

Small Cap = The wild entrepreneur

Full of potential, but one wrong step can change everything.

Now here’s the twist:

Most people think they should “graduate” from small to large caps as they age. But reality? Many experienced investors still allocate to small caps. Not because they are risky takers but because they understand cycles.

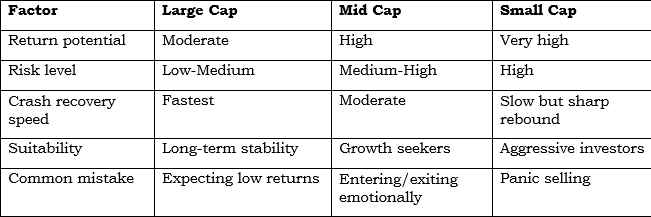

Large cap safety is often an illusion of stability.

Large caps feel safe because they fall less… not because they don’t fall. During market stress, they still fall. Just slower. And slower pain often tricks investors into staying longer than they should or ignoring underperformance. Sometimes slow-moving losses in large caps hurt wealth creation more than sharp corrections in small caps, because investors don’t even realise opportunity cost.

Mid caps are the “compounding accelerators” of the market

Mid caps rarely get attention in headlines. That’s exactly why they behave differently. They are in transition, expanding businesses, improving margins, entering new markets. If large caps are highways, mid caps are express lanes under construction. But construction roads are bumpy. And most investors quit midway.

Small caps don’t fail; investors timing does. Small caps are misunderstood.

People assume:

“Small cap = risky = avoid”

But the real truth is:

Small caps fail not because they are small, but because investors treat them like large caps emotionally. They expect stability from instability. And when volatility comes, they exit too early.

WHAT HAPPENS DURING A MARKET CRASH? (COVID 2020 REALITY CHECK)

Let’s go back to March 2020.

Markets crashed sharply. Panic everywhere. News channels flashing red. Investors checking portfolios every hour. Now observe what happened across categories:

Large Caps: Fell, but relatively controlled. Recovery started earlier. Institutional support was stronger.

Mid Caps: Fell harder. Recovery was delayed. Many stocks took longer to regain pre-crash levels.

Small Caps: Fell the most brutally. Some stocks collapsed 50–70%. But interestingly, some also became multi-baggers in the recovery phase.

Now here’s the psychological reality: Most investors didn’t lose money in the crash.

They lost money in the exit during the crash. The biggest wealth destruction during COVID was not the fall; it was selling mid-cap and small-cap funds at the bottom and never re-entering.

THE BIGGEST MYTH ABOUT LARGE CAP SAFETY

Let’s break something that most people believe blindly:

“Large caps are always safe investments.” No.

Large caps are relatively stable, not immune. They can underperform for years when growth cycles favour mid and small caps. Safety in investing is not about category. It is about alignment with time horizon.

A 2-year investor in small caps feels pain.

A 15-year investor in small caps often sees wealth creation.

Same asset. Different outcome.

WHY SOME SMALL CAPS BECOME WEALTH CREATORS (AND MOST DON’T)

This is where most blogs oversimplify. Small caps are not wealth creators by default. They become wealth creators when three things align:

1. Business survives competition

2. Management executes consistently

3. Investor stays invested through volatility

The third point is the most ignored. Because wealth creation is not about buying right. It is about staying right.

INVESTOR PERSONALITY TYPES: WHERE DO YOU REALLY BELONG?

Let’s go beyond income and age.

1. Stability-first investor

• Prefers predictability

• Panics during volatility

Large Caps suit you

2. Growth-balanced investor

• Comfortable with moderate swings

• Wants both safety and upside

Mid Caps suit you

3. High-risk opportunity seeker

• Enjoys volatility

• Thinks long-term in stories, not charts

Small Caps suit you

But here’s the truth nobody says: You are not one personality forever. You evolve with experience, losses, and market exposure.

COMPARISON TABLE 1: THE WAY YOUR MIND SHOULD SEE THEM

COMPARISON TABLE 2: WHAT ACTUALLY MATTERS FOR WEALTH CREATION

Diversification is not splitting money; it is splitting emotions. Most investors think diversification means “put money everywhere.”

Wrong.

True diversification means: Balancing how you will feel in different market conditions. Because emotions decide returns more than selection.

The best portfolio is not the highest-returning one it is the one you can survive.

A portfolio that gives 15% but you can stay invested in is better than a portfolio that gives 25% but you exit during volatility. Survival beats optimisation in real markets.

So… which is best? – Wrong question.

The real question is:

Are you building a portfolio that matches your patience, or your ambition?

Because markets don’t punish wrong choices. They punish wrong behaviour.

FINAL THOUGHTS: THE UNCOMFORTABLE TRUTH

Large cap will not make you rich quickly.

Small cap will not make you rich safely.

Mid cap will not protect you emotionally.

But together, they might do something more powerful: Help you stay invested long enough for compounding to work. And compounding only rewards one thing.

Consistency over emotion.

Before you invest next time, ask yourself:

“Am I choosing this fund… or am I choosing how I want to feel during the next crash?”

Look at your current portfolio. Is it aligned with your goals or just a reflection of past market hype?

Take 10 minutes today to understand how each market cap behaved during the last 5 major market cycles. Patterns repeat more than predictions.

Track your last 3 investment decisions.

Were they based on logic or recent market emotions?

If building a balanced long-term portfolio feels confusing, having structured guidance and disciplined investing support can sometimes matter more than picking the “right” category alone.

So, in markets, the biggest risk is not choosing the wrong category; it is choosing without understanding your own behaviour.

Disclaimer

What's Trending

Build Wealth in Your 20s: Simple Investing Guide for Indians

January 27, 2026

Meesho, Aequs & Vidya IPOs: Will They Pop on Listing?

December 3, 2025

The Evergreen Portfolio: Building a Retirement That Blooms

December 8, 2025

Equity vs. Shares: Understanding the Key Differences

January 5, 2024

Recent Blog

.jpeg)

Blog

Recent Blogs

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.