.jpeg)

India's Population Is Changing. Is Your Money Ready?

Picture a typical family gathering.

Too much food on the table. Someone insisting you eat more. And eventually, the question every young adult in India has heard at least once:

"So… when are we hearing good news?"

You laugh. Someone makes a joke. You change the subject.

But tucked inside that casual conversation is something much bigger — something that's been reshaping India quietly for years.

For decades, the worry was about too many people. Too much pressure. Too many mouths to feed.

Then something shifted.

Families got smaller. People started living longer. And suddenly the conversation stopped being about how many people India has — and started being about who those people are, and what that means for all of us financially.

Because demographic shifts don't stay inside economics papers. They show up in your rent. Your parents' hospital bills. Your retirement account. Your future.

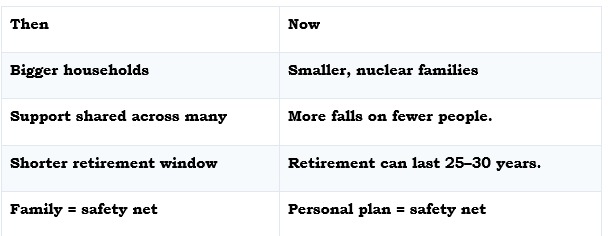

The Shift Is Already Here

Look around. Many of our parents grew up in larger families where costs and responsibilities were shared across more people.

That's changing fast.

Not because people care less about family. Life simply became more expensive. Housing. Education. Healthcare. Even groceries feel heavier on the budget than they did a generation ago.

For many people today, deciding when — or whether — to grow a family is as much a financial decision as a personal one.

That creates a quiet but permanent change in how a country works.

India's Demographic Story at a Glance

Nothing happens overnight. But slowly the balance tips — and eventually, your money starts feeling it.

What This Means for You

1. Retirement May Last Much Longer Than Your Parents Expected

There was a time when retirement meant slowing down for a few years, with family handling the rest.

Today, many people could spend 25 to 30 years in retirement.

That sounds wonderful — until you do the numbers.

Your salary stops. Your expenses don't.

Longer life means more years to fund, more inflation to absorb, more medical costs to manage. It shifts the question from "How much should I save?" to "How long should my money last?" — and those require very different answers.

Starting a SIP at 25 versus 35 can mean the difference of several lakhs by the time you retire — the earlier you start, the less you have to put in each month to reach the same number. Platforms like GoPocket make it straightforward to set up automated investing so the habit runs on its own.

2. Healthcare Is No Longer a Backup Plan

Try answering this honestly: if a medical emergency happened tomorrow — would your current savings absorb it? Not after selling something. Not after borrowing. Just from your own plan.

Most people push healthcare protection to later. Then later arrives.

And by the time you really want it, premiums are higher, and coverage is trickier to get.

The goal isn't to scare yourself. The goal is to give yourself options. A decent health insurance plan secured in your 30s is far cheaper — and far more accessible — than one you scramble for in your 50s.

3. The Family Safety Net Has Quietly Changed

For a long time, Indian families operated like informal insurance. Someone always stepped in. Costs got shared. Responsibilities spread across siblings, cousins, parents.

That support still exists. But life looks different now.

People move cities. Families become smaller. Parents live longer. One or two people often carry far more financial responsibility than earlier generations did.

Financial independence isn't becoming more important because people are becoming individualistic. It's becoming important because life itself has changed.

4. Big Shifts Create Long-Term Opportunities Too

Here's the part most people miss.

Population shifts don't just affect households — they reshape industries. As India ages and urbanises, certain sectors tend to see sustained, structural demand:

• Healthcare and diagnostics

• Insurance and financial services

• Wealth management and retirement products

• Automation and digital services

This isn't about chasing sectors or timing markets. It's about recognising that long-term demographic trends create long-term investment themes — worth understanding even if you're building a simple SIP portfolio.

What Can You Actually Do Today?

Nothing dramatic. You don't need a financial overhaul.

• Start retirement investing earlier than feels necessary — even small amounts compound significantly over decades

• Review your health insurance before you need it, not after

• Automate your investing so consistency doesn't depend on motivation

• Keep building skills — adaptability is one of the highest-return investments you can make

Small actions repeated for years beat big plans delayed forever.

Your 5-Minute Money Check

☐ Am I planning for a retirement that could last 25+ years?

☐ Have I increased my SIP recently?

☐ Is my health insurance adequate for today's costs?

☐ Do I have 3–6 months of emergency savings?

☐ Have I had an honest money conversation with my family?

One Last Thought

Demographic shifts don't arrive with loud headlines. They come quietly. One household at a time. One financial decision at a time.

And then one day, you realise the world works differently than it did for your parents.

You can't control what direction a country's population moves. But you can prepare for the world it's building — and preparation has always been one of the simplest forms of financial freedom.

GoPocket — Money, Made Simple. Wealth, Built for the Long Run.

⚠ Disclaimer

Investments are subject to market risks. Please read all scheme-related documents carefully before investing. This content is for educational purposes only and does not constitute investment advice. GoPocket is a SEBI-registered intermediary.

Disclaimer

What's Trending

The trading jar of emotions : 8 Feelings that control every trader

November 1, 2025

Oil Crisis 2026: Why Your LPG Bill Just Went Up ₹60

March 27, 2026

Recent Blog

.jpeg)

Open your GoPocket Account within 5 minutes.

Have any queries?

Get support

Investing and trading is made simple, affordable and accessible for every Indian.

© Made with ❤️ in Coimbatore, India | Copyright © 2023 onwards, GoPocket.